was developed by Box and Jenkins. The default automatic determination of

the best model order in SigmaXL uses the stepwise method of Hyndman

and Khandakar (see fpp2).

Stationarity, Differencing and Constant

ARIMA assumes that the time

series is stationary, i.e., it has the

property that the mean, variance and autocorrelation structure do

not change over time. If a time series mean is not stationary (e.g.

trending), this can be corrected by differencing, computing the

differences between consecutive observations for nonseasonal and

between consecutive periods for seasonal data (e.g., Jan 2019 Jan

2018, etc.). For nonseasonal, this will typically involve 1 or 2

orders of differencing. This order is the Integrated term d. For

seasonal, this will typically involve 1 order of differencing. This

order is the Seasonal Integrated term D. A constant term c is

optional:

If d+D=0, a constant term in the model is the mean. If d+D=1, a constant

term in the model is a trend (drift). If d+D>1, a constant term would be a quadratic

or higher trend, so

constant should not be included. It is recommended that d+D should not be > 3. If

the variance is not stationary, use a Box-Cox transformation.

Autoregressive (AR) Model

In an autoregressive model, we forecast the variable of interest using a linear combination

of past values of the variable.

The term autoregressive indicates that it is a regression of the variable against itself:

where 𝜀t is white noise. This is like a multiple regression but with

lagged values of

yt as predictors.

We refer to this as an AR(p) model, an autoregressive model of order p

(fpp2).

Moving Average (MA) Model

Rather than using past values of the forecast variable in a regression, a moving average

model uses

past forecast errors in a regression-like model:

We refer to this as an MA(q) model, a moving average model of order q

(fpp2).

Autoregressive Integrated Moving Average (ARIMA) Model

If we combine differencing with autoregression and a moving average model, we obtain a

nonseasonal ARIMA model:

where 𝑦𝑡′ is the differenced series. This ARIMA (𝑝, 𝑑, 𝑞) model, where 𝑝 is

the number of

autoregressive terms, 𝑑 is the degree of differencing and 𝑞 is the number of moving

average terms.

Seasonal ARIMA

For seasonal, the model consists of terms

that are similar to the nonseasonal components of the

model, but include the seasonal components. The seasonal model is ARIMA (𝑃,𝐷,𝑄) and

combined we have ARIMA (𝑝, 𝑑, 𝑞) (𝑃,𝐷,𝑄).

ARIMA Model Order

Model order may be automatically determined or user specified. The Stepwise Procedure

utilizes

the stepwise method of Hyndman and Khandakar (see Appendix:

Automatic

Model Selection): Seasonal 𝐷 (0 or 1) is determined using a Seasonal Strength test,

or user specified.

Nonseasonal 𝑑 (0, 1, or 2) is determined using a modified KPSS unit root test, or

user specified.

AR (𝑝), MA (𝑞), with orders from 0 to a maximum of 5.

Seasonal, SAR (𝑃), SMA (𝑄), with orders from 0 to a maximum of 2.

Constant (included or not included) if 𝑑 + 𝐷 ≤ 2; not included if 𝑑 + 𝐷 > 2.

An Extended Model Search will search over the same range of order

values as Stepwise but do so

using all combinations, subject to the following constraints for consistency and

computational

efficiency:

𝑑 and 𝐷 are determined using the same methods as Stepwise, or specified by the

user.

Constant (included or not included) if 𝑑 + 𝐷 ≤ 2; not included if 𝑑 + 𝐷 > 2.

𝑝 + 𝑞 + 𝑃 + 𝑄 ≤ 7.

Computation time limit is specified by user.

In general, the default Stepwise Procedure is

recommended over the

Extended Model Search, as it

is much faster and usually finds the best ARIMA model, or a simpler one that is close to

the best

ARIMA model.

Model Parameter Estimation and Missing Values

Model parameters are solved using nonlinear maximization of the Log-Likelihood function. Two

general models are available - the conditional sum of squares (CSS) and the state space

Kalman maximum likelihood. The CSS is always used for initial estimates and is used if

n > 500 or seasonal frequency > 12 for computational efficiency. Kalman

Filters permit exact calculations and can handle missing values. For CSS, if missing values

are encountered, the largest contiguous range is used.

For further details and formulas, see Appendix: Autoregressive Integrated Moving Average - ARIMA.

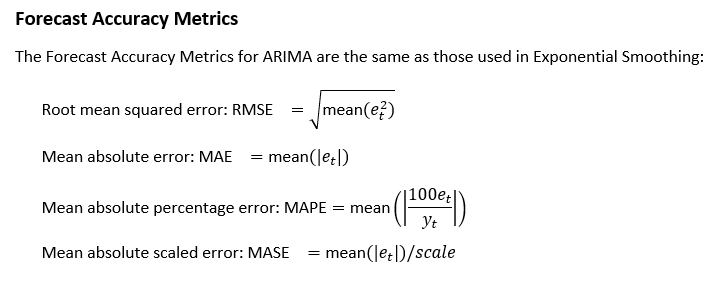

ARIMA Model Statistics and Information Criteria for Model Comparison

The ARIMA model statistics are similar to those used in Exponential Smoothing.

Log-Likelihood is related to -Ln(Sum-of-Squares Error), so is maximized. Information

Criteria AICc, AIC and BIC are calculated using -2*Log-Likelihood and incorporate a penalty

for the number of terms in the model, so smaller is better. These are used in automatic

model selection. AICc is the default Information Criterion, based on forecast error

performance with competition data.

For further details, see Information Criteria for Model

Comparison.

Open Chemical Process Concentration Series A.xlsx

(Sheet 1 tab). This is the Series A data from

Box and Jenkins, a set of 197 concentration values from a

chemical process taken at two-hour intervals. See the Run Chart,

ACF/PACF Plots, Spectral.html and Seasonal Trend

Decomposition Plots for this data.

Click SigmaXL > Time Series

Forecasting > ARIMA Forecast > Forecast. Ensure that

the entire data table is selected. If not, check Use

Entire Data Table. Click Next.

Select Concentration, click

Numeric Data

Variable (Y) >>. Check Display

ACF/PACF/LB Plots and Display Residual Plots.

Leave Specify Model Periods, Seasonal Frequency

and Box-Cox Transformation unchecked. We will

use the default No. of Forecast Periods = 24

and Prediction Interval = 95.0 %.

Optional Time Axis Labels will be displayed on the forecast

chart time axis. If used, dates for the forecast periods should

also be included, otherwise the time axis will be blank for the

forecast periods.

No. of Forecast Periods are the number of time series values

to be predicted (forecast horizon). The most accurate forecast

will be for the first predicted value (one-step-ahead).

Prediction Interval % is the confidence level for the

individual predictions. For example, a 95% prediction interval

contains a range of values which should include the actual

future value with 95% probability. The interval will get larger

the further out you predict.

Model Options opens another dialog which allows you to set

automatic options or to specify a model.

Display ACF/PACF/LB option will produce ACF

and PACF plots for the raw data as well as for the model

residuals. The LB plot is a plot of Ljung-Box test P-Values for

various lags and is used to determine if a group of

autocorrelations are significant, (i.e., the autocorrelations do

not come from a white noise series). For further details, see

Ljung-Box Test.

Display Residual Plots will produce a table of model residuals

and the usual model residual plots: histogram, normal probability plot, residuals

versus data order, and residuals vs forecast value. Note that if a Box-Cox

transformation is applied, the residuals are transformed so will not be equal to

forecast - actual.

Specify Model Periods are used to specify a start period, end

period or withhold sample. The withheld data is not used in model estimation, so

this is very useful for model validation and comparison. This will be used in a

later example.

Seasonal Frequency and Box-Cox Transformation

will be used in a later example.

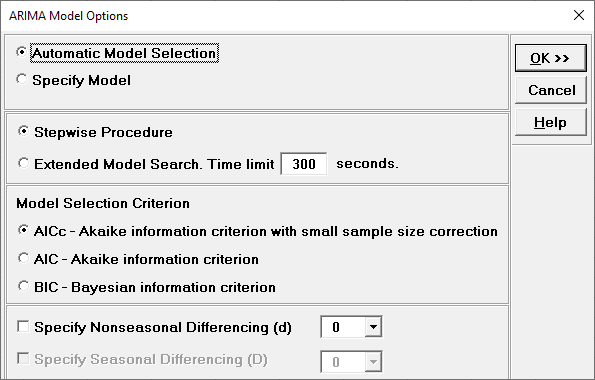

Click Model Options.

Automatic Model Selection will be used later. It is the default

selection.

Extended Model Search is described above. The Time limit may need to be increased for

seasonal models with high seasonal frequency and/or large number of observations.

Model Selection Criterion is the information criterion metric to be

used in automatic model selection. AICc is the default selection.

Specify Nonseasonal Differencing (d) = 0, 1, or 2, overrides the

automatic nonseasonal differencing. This is useful to compare models for borderline

cases that are nearly nonstationary (see Box and Jenkins).

Specify Seasonal Differencing (D) = 0 or 1, overrides the automatic

seasonal differencing. It is greyed out here because

Seasonal Frequency was unchecked in the previous dialog.

Clicking OK accepts the settings and returns you to the previous

dialog. Clicking

Cancel will cancel any changes and return you to the previous

dialog.

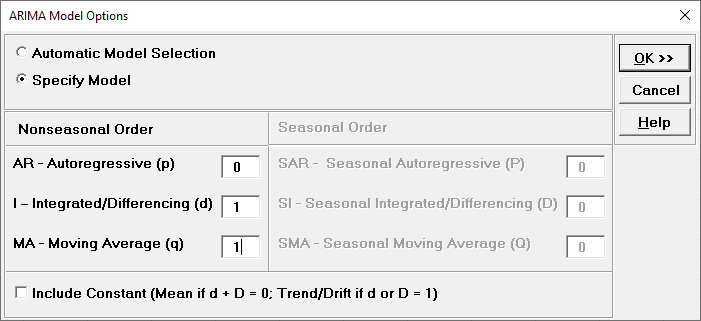

Select Specify Model.

Specify Nonseasonal Order I Integrated/Differencing

(d) = 1 and MA Moving Average (q) =

1. Leave Include Constant unchecked.

Specify Model allows you to manually specify the

Nonseasonal Order and Seasonal Order values and option

for

Include Constant (Mean if d + D = 0; Trend/Drift if d or D = 1). If d +

D = 0, then the constant term is the mean; if d or D = 1, then the constant term is a

Trend; if d + D > 1, then the constant term is quadratic or higher this is not

recommended.

Seasonal Order is greyed out because Seasonal

Frequency was unchecked in the previous dialog.

The specified ARIMA (0,1,1) is equivalent to a simple exponential smoothing model (with

slight differences due to estimation of the initial value).

Click OK to return to

the ARIMA Forecast dialog. Click OK. The ARIMA

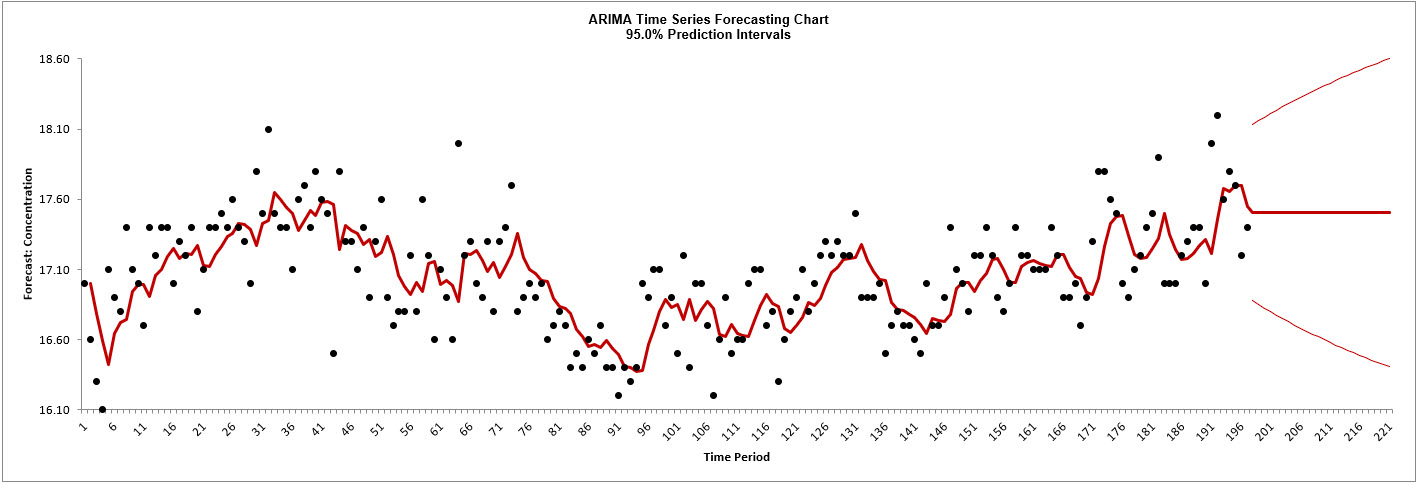

forecast report is given:

As expected, this is very similar to the exponential smoothing

forecast chart that was produced using the Simple

Exponential Smoothing with Additive Errors (A, N, N)

Exponentially Weighted Moving Average (EWMA) model. The

initial in-sample predicted value for ARIMA is slightly

different and starts at the second time period due to

differencing.

Scroll down to view the ARIMA Model

header:

If we had checked Specify Model Periods in the main dialog, the

start, end or withhold selection would be summarized here as

well.

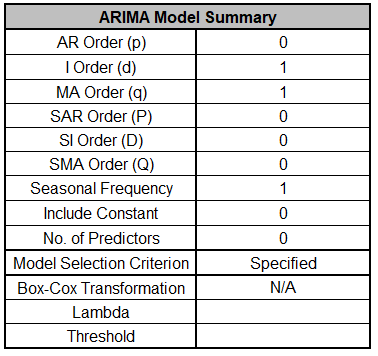

The ARIMA Model Summary is given as:

This is a summary of model information: ARIMA (0,1,1) with no

constant and no predictors. Seasonal Frequency = 1

(nonseasonal); Model Selection Criterion = Specified because

the model was user specified; and Box-Cox Transformation = N/A

because Box-Cox Transformation was unchecked.

The Parameter Estimates are:

The MA_1 parameter coefficient value is approximately equal to 1 alpha = 1 - 0.2948 =

0.7052 in Exponential Smoothing

Parameter Estimates. The slight difference is due to estimation of the initial

value.

ARIMA Parameter Estimates include significance tests; P-Values < .05 are significant

and highlighted in red. This may be useful for model refinement with multiple predictors

(and will be demonstrated later). Note that for AR/MA model order selection, minimum

AICc should be used, rather than significance tests (see Kostenko, A.V. and Hyndman, R.J.).

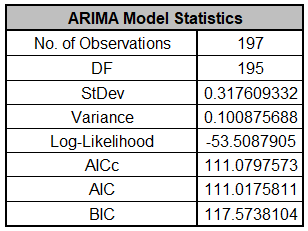

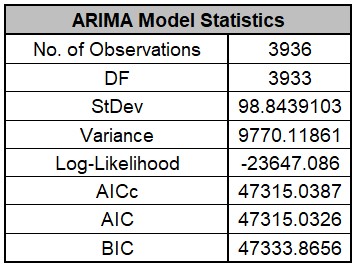

Comparing to the Exponential Smoothing Model Statistics, we see

that the StDev and Variance are approximately equal, but the

Log-Likelihood, AICc, AIC and BIC are very different. This is

due to different formulas being used in the Likelihood function.

You cannot use Information Criteria to compare ARIMA and

Exponential Smooth models to determine which model has the best

fit.

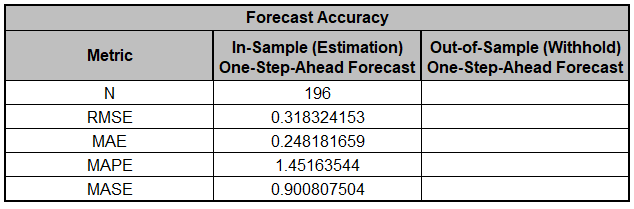

The In-Sample Forecast Accuracy metrics

are:

MASE is less than one, so it is a better forecast than would be obtained from a nave

forecast (set all forecasts to be the value of the last observation).

See Forecast Accuracy Metrics.

These are

the same forecast and prediction interval values displayed in the Forecast Chart but

provided for further analysis or charting. If Withhold Periods are specified, the

Withhold Data will be displayed as well.

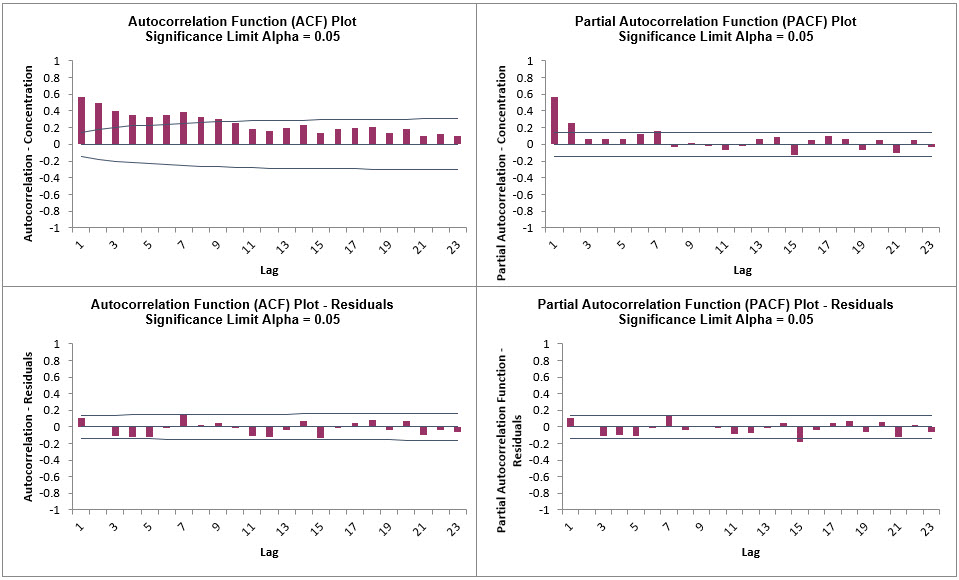

Click on the ARIMA ACF PACF

LB sheet to view the ACF/PACF/LB Plots:

These are approximately the same as what we obtained previously with Exponential Smoothing ACF/PACF/LB

Plots. We can see that all of the autocorrelation has been removed by the

exponential smoothing model (with the exception of lag 15 in the PACF), so this is a

good fit to the time series data.

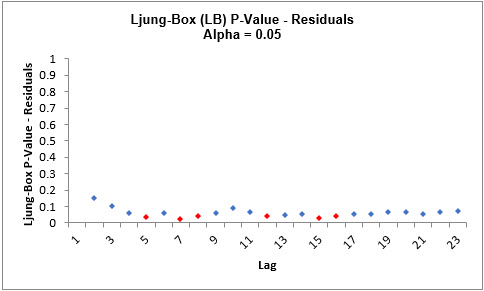

The LB plot is a plot of Ljung-Box test P-Values for various lags and is used to

determine if a group of autocorrelations are significant, (i.e., the autocorrelations do

not come from a white noise series).

For further details, see Ljung-Box Test.

The red P-Values are significant (alpha=.05) and the blue P-Values are not significant.

It is desirable that all P-Values be blue. The ACF/PACF plots indicated that almost all

of the correlation has been accounted for in the model, but the Ljung-Box plot shows

that some significant autocorrelation still remains - so the model can potentially be

improved. This does not mean that the model is a bad model, it can still be very useful

for prediction purposes, but the prediction intervals may not provide accurate

coverage.

There does appear to be fewer significant P-Values than we obtained previously with the

Exponential Smoothing LB plot,

but this may not be a practical difference, given the similarity of all the other

statistics.

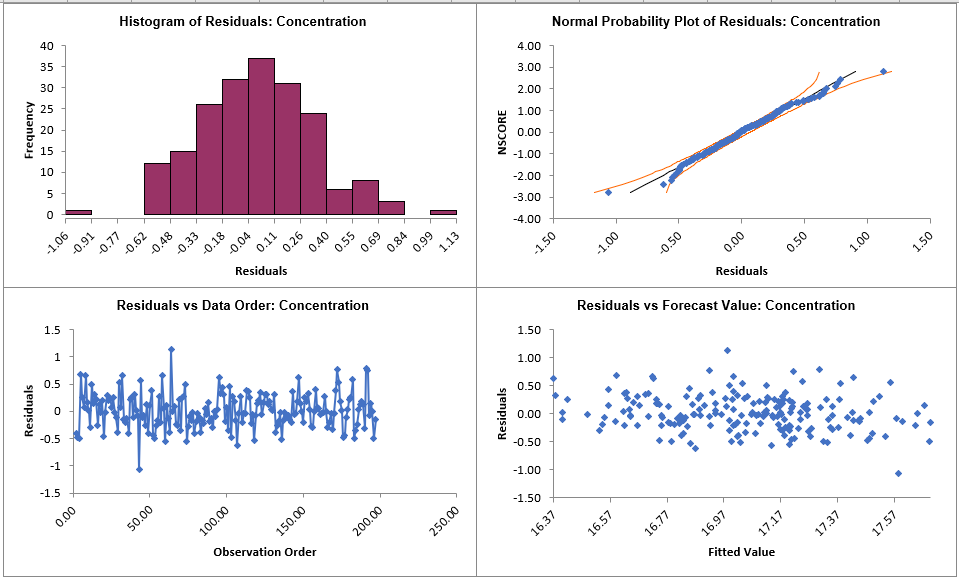

Click on the ARIMA Residuals

sheet to view the Residual Plots:

The residuals are approximately normally distributed, with a

roughly straight line on the normal probability plot.

There are no obvious extreme outliers or patterns in the charts. Later, we will apply a

control chart to the residuals to formally test for significant outliers or assignable

causes.

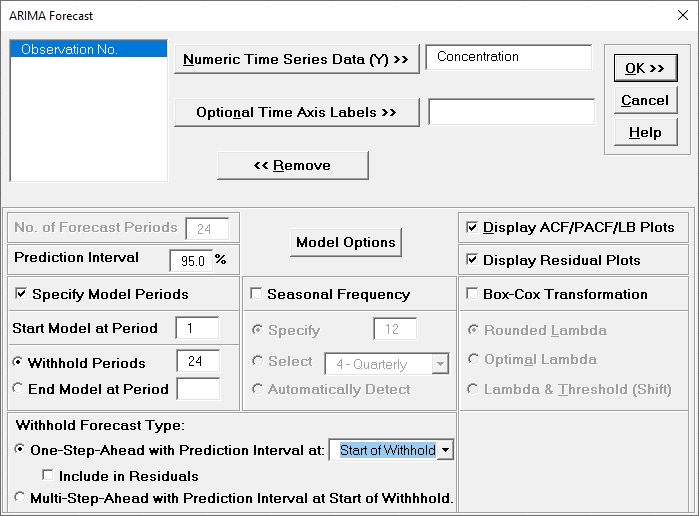

Now we will rerun ARIMA Forecast on the

Concentration data with Automatic Model Selection and Specify

Withhold Periods. Click Recall SigmaXL Dialog

menu or press F3 to Recall Last Dialog. Check

Specify Model Periods. Set Withhold

Periods = 24. We will use the default Withhold

Forecast Type: One-Step-Ahead with Prediction Interval at:

Start of Withhold.

Specify Model Periods option allows you to specify the start

and end periods used in automatic model identification and

parameter estimation. Typically, Start Model at Period is kept =

1 and Withhold Periods specifies the number of periods to be

withheld for out-of-sample testing. End Model at Period

specifies the end period, so the withhold sample size would be:

total number of observations end period.

Withhold Forecast Type: One-Step-Ahead will exclude the

withhold sample from automatic model identification and

parameter estimation, but uses the withhold data to update the

predicted one-step ahead forecast. This is useful to assess

forecast error when you only care about the short-term one-step

ahead prediction.

Withhold Forecast Type: One-Step-Ahead with Prediction

Interval at: Start of Withhold will display the prediction

interval for the duration of the withhold sample. Note that the

length of the prediction interval is determined by the number of

withhold periods, so overrides the specified No. of Forecast

Periods.

Withhold Forecast Type: One-Step-Ahead with Prediction

Interval at: End of Withhold will display the prediction

interval at the end of the withhold sample. The length of the

prediction interval is determined by the specified No. of

Forecast Periods.

Include in Residuals will treat the one-step-ahead forecast

errors as residuals (even though they were not part of the model

estimation process) and will be included in the ACF/PACF/LB

Residual Plots along with the Residuals report and graphs.

Typically, this is kept unchecked.

Withhold Forecast Type: Multi-Step-Ahead with Prediction

Interval at Start of Withhold will exclude the withhold sample

from automatic model identification and parameter estimation and

does not use the withhold data to update the predicted one-step

ahead forecast. This is useful to assess forecast error when you

are interested in a long-term forecast window (horizon). The

prediction interval will be displayed for the duration of the

withhold sample. Note that the length of the prediction interval

is determined by the number of withhold periods, so overrides

the specified No. of Forecast Periods. These forecast errors are

not included in ACF/PACF/LB Residual Plots or the Residuals

report and graphs.

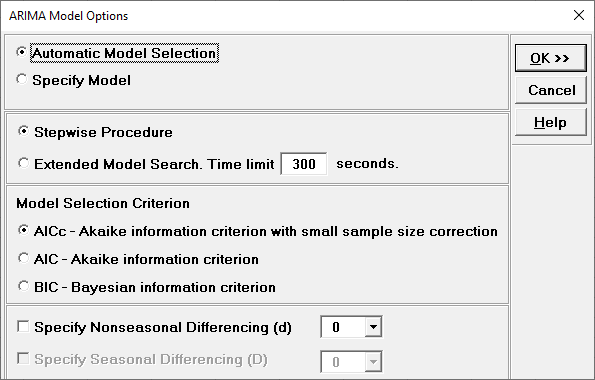

Click Model Options.

Select Automatic Model Selection. We will use

the defaults: Stepwise Procedure and Model Selection Criterion:

AICc Akaike information criterion

with small sample size correction, leave Specify Nonseasonal

Differencing (d) unchecked.

Tip: When using Recall SigmaXL Dialog and if there are

no changes to the

Model Option settings, the previous settings will be used. It is not

necessary to repeat this step.

Click OK to return to

the ARIMA Forecast dialog. Click OK. The ARIMA

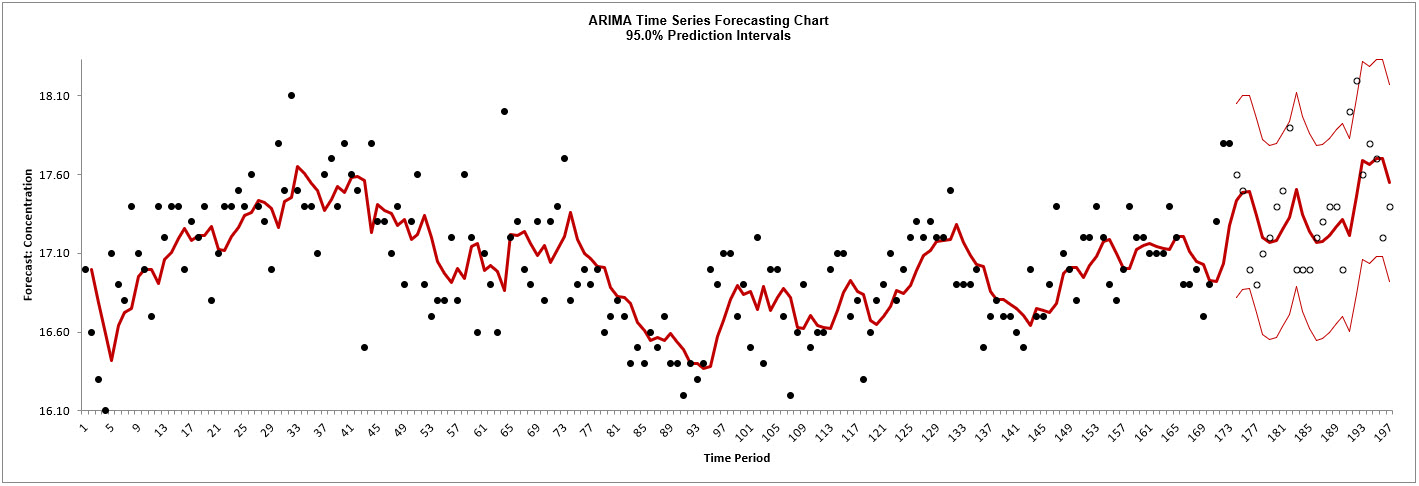

forecast report is given:

The blank dots are the data values in the withhold sample with a one-step-ahead forecast

and prediction intervals displayed at the start of the withhold sample.

This is very similar to the exponential smoothing forecast chart that was produced using the

Simple Exponential Smoothing with Multiplicative Errors (M, N, N) model. The initial

in-sample predicted value for ARIMA is slightly different and starts at the second time

period due to differencing.

Scroll down to view the ARIMA Model header:

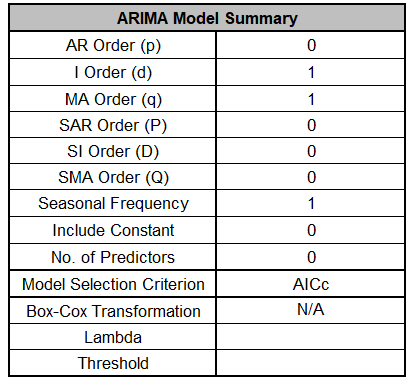

The ARIMA Model Summary is given as:

The ARIMA

(0,1,1) model that we manually specified above, was also automatically selected based on

the AICc criterion.

The Parameter Estimates are:

This is close to the parameter estimate obtained above (which used

all of the data).

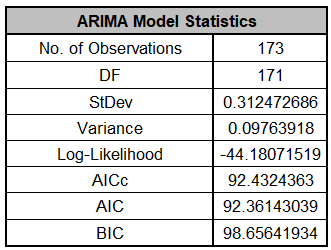

The ARIMA Model Statistics are:

These are fairly close to the model statistics obtained above

using all of the data. Here we are using only 173 of the 197 observations.

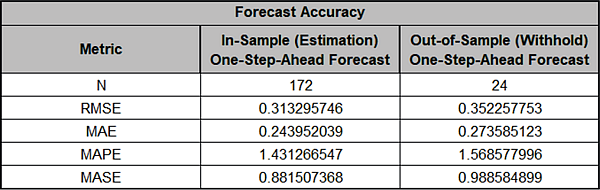

The Forecast Accuracy metrics are:

As expected, the Out-of-Sample (Withhold) One-Step-Ahead

Forecast errors are larger than the In-Sample (Estimation)

One-Step-Ahead Forecast errors.

These are very similar to the Exponential Smooth Forecast

Accuracy Metrics that were produced using the Simple Exponential

Smoothing with Multiplicative Errors (M, N, N) model. Note that

we lose one observation on the In-Sample (N=172) since we do not

have a predicted value at time period = 1 due to differencing.

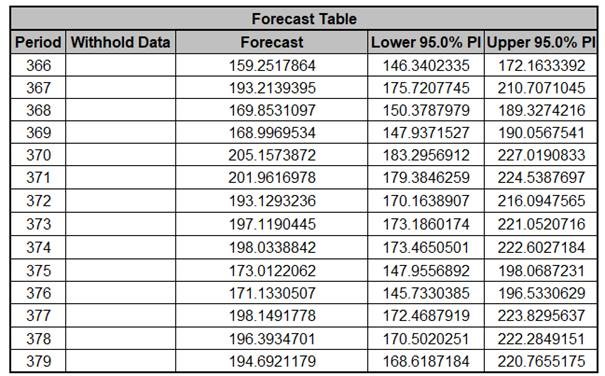

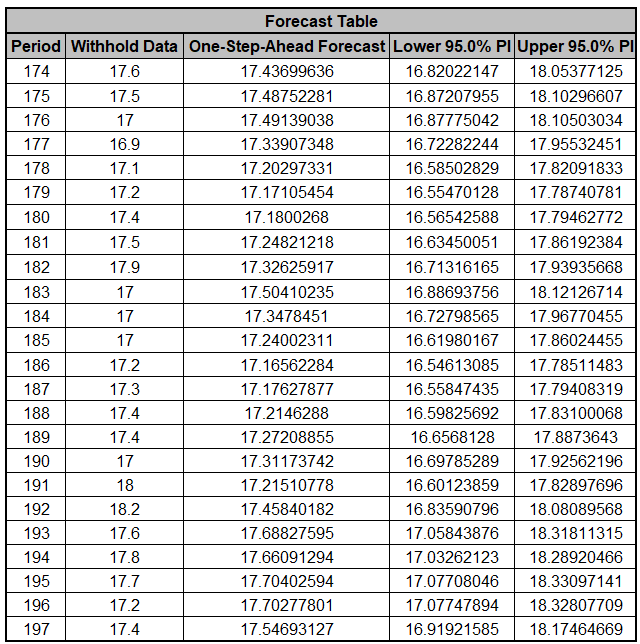

The Forecast Table is given as:

These are the same forecast and prediction interval values

displayed in the Forecast Chart, but provided for further

analysis or charting. The Withhold Data is also

displayed.

The ACF/PACF/LB Residual Plots and

Residual Plots are based on the in-sample data. The plots look

similar to the complete data above, except for the Ljung-Box

P-Values:

As was the case with exponential smoothing, the ARIMA (0,1,1) model is a better fit

to the subset than the complete data, with all P-Values being blue (> .05).

If Include in Residuals

was checked then the residuals would also include the Out-of-Sample (Withhold)

One-Step-Ahead Forecast

errors.

The above analysis can be rerun using

Withhold Forecast Type: Multi-Step-Ahead with Prediction

Interval at Start of Withhold (click Recall

SigmaXL Dialog menu or press F3 to Recall Last Dialog),

but we will not do so here. The results would be very similar to

those obtained with exponential smoothing.