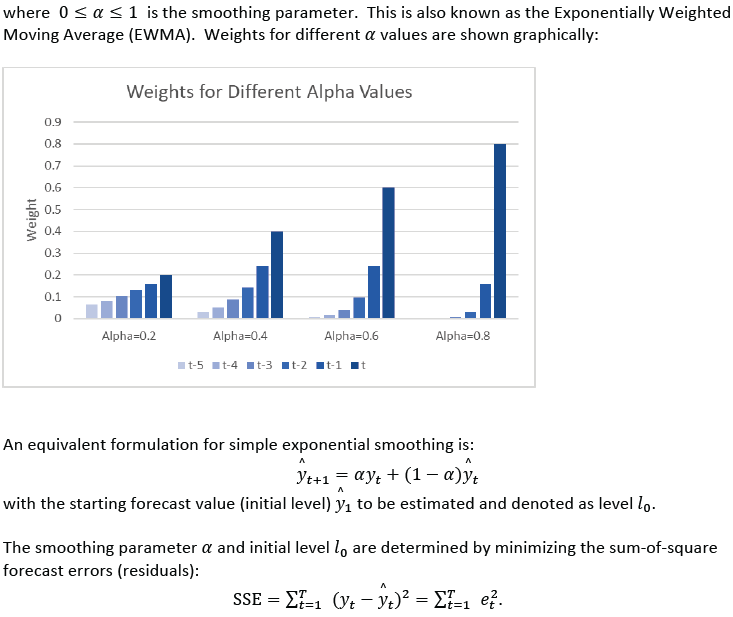

Simple Exponential Smoothing forecasts are calculated using weighted averages, where the

weights decrease exponentially as observations come from further in the past with the

smallest weights associated with the oldest observations:

Error, Trend, Seasonal (ETS) Models

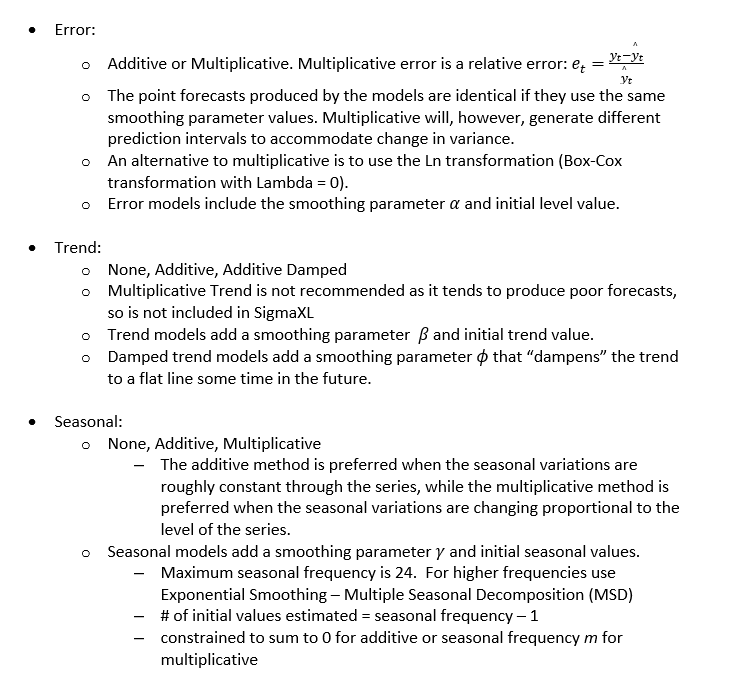

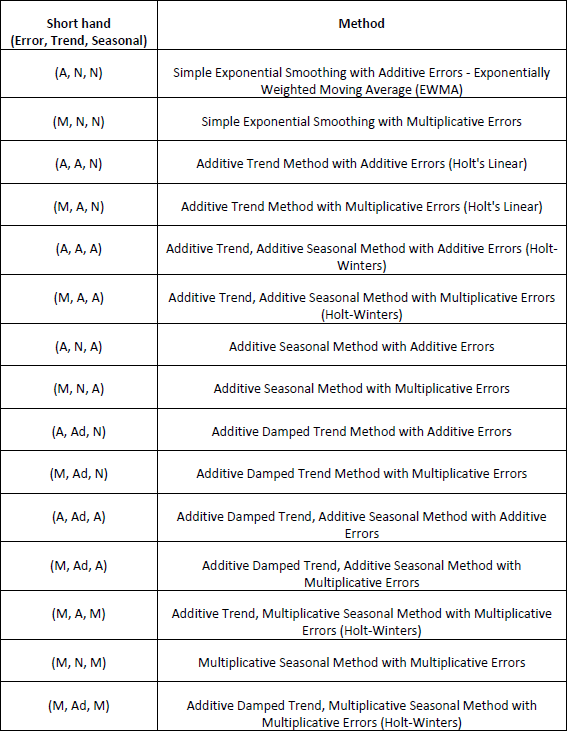

Error, Trend, Seasonal (ETS) models expand on simple exponential smoothing to accommodate

trend and seasonal components as well as additive or multiplicative errors. Simple

Exponential Smoothing is an Error Model. Error, Trend model is Holts Linear, also known as

double exponential smoothing. Error, Trend, Seasonal model is Holt-Winters, also known as

triple exponential smoothing. Rob Hyndman has developed a complete taxonomy that describes

all of the combinations of exponential smooth models in a consistent manner (see fpp2):

Exponential Smoothing Parameter Estimation, Model Statistics and Information Criteria for

Model Comparison

Model parameters are solved using nonlinear maximization of the Log-Likelihood function.

Log-Likelihood is related to -Ln(Sum-of-Squares Error). Information Criteria AICc, AIC and

BIC are calculated using -2*Log-Likelihood and incorporate a penalty for the number of terms

in the model, so smaller is better. These are used in automatic model selection. AICc is the

default Information Criterion, based on forecast error performance with competition data.

Missing Values

Exponential Smoothing handles missing values with seasonally adjusted linear interpolation.

While there is robustness against some missing values, if the number of missing values is

large then model estimation and forecast accuracy will be degraded. Upon selection of a time

series with missing values, you will see a pop-up Warning: Missing values detected.

Seasonally adjusted linear interpolation will be used.

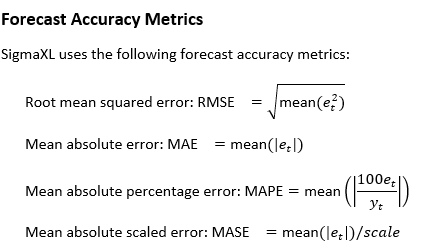

where scale is the MAE of the in-sample nave or seasonal nave forecast (set all forecasts

to be the value of the last observation/period). Note that scale for nonseasonal is

identical to MR-bar of an Individuals Moving Range chart. A scaled error is less than one if

it arises from a better forecast than the average nave/seasonal nave forecast. Conversely,

it is greater than one if the forecast is worse than the average nave forecast. MASE is

recommended over the popular MAPE, because MAPE becomes infinite if any y_t=0.

In-Sample is also referred to as the Train data. The same metrics may be applied to

Out-of-Sample (Withhold), also referred to as the Test data and may be One-Step-Ahead or

Multi-Step-Ahead. This will be demonstrated later. Out-of-Sample (Withhold) data is not used

in the model parameter estimation, so is a much better indicator of true forecast accuracy.

In-sample accuracy metrics can be biased due to overfitting. Scale is always computed using

the in-sample data.

Demo of Simple Exponential Smoothing Concentration

Open Demo of Simple Exponential Smoothing

Concentration.xlsx (Sheet 1 tab).

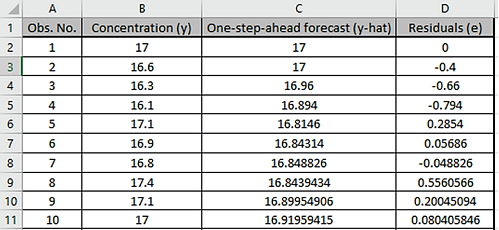

This is the Series A data from Box and Jenkins, a set of 197 concentration values from a

chemical process taken at two-hour intervals in Column B.

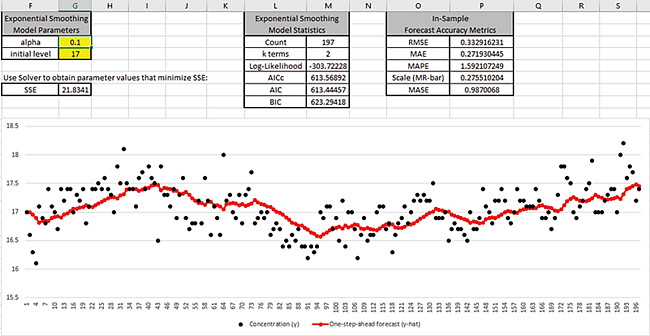

Cell G3 is the alpha smoothing parameter value, cell G4 is

the initial level. These may be manually entered or solved with Solver.

The One-step-ahead forecast is calculated as follows: C2 is the initial level value; C3

=alpha*B2+(1-alpha)*C2; C4 =alpha*B3+(1-alpha)*C3, etc.

Cell G7 is the Residuals Sum-of-Squares error and is the value to be

minimized, in order to produce the most accurate one-step-ahead forecast.

The exponential smooth model statistics are also given for later comparison to the SigmaXL

report.

The raw Concentration data are the black dots in the graph; the one-step-ahead forecast

values are the red dots.

Model Statistics and Forecast Accuracy Metrics will be discussed later.

Before we use Solver to determine the optimal alpha and initial

level values, we will manually enter some values to see how the graph changes.

Enter alpha = 0.01 as shown:

This small value of alpha produces a smooth fit with SSE = 31.02 that is larger than what we

started with (SSE = 21.83).

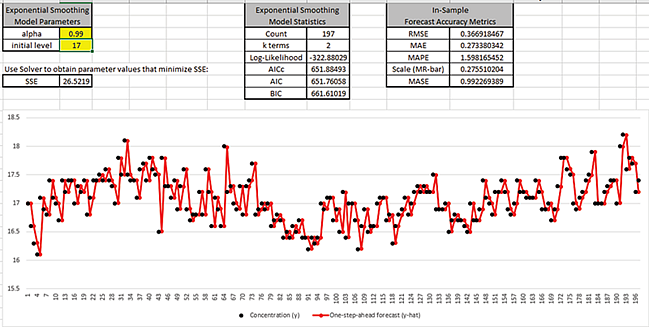

Now enter alpha = 0.99 as shown:

This large value of alpha results approximately in a nave forecast, with the one-step-ahead

forecast value equal to the previous actual. SSE = 26.52 is larger than what we started

with.

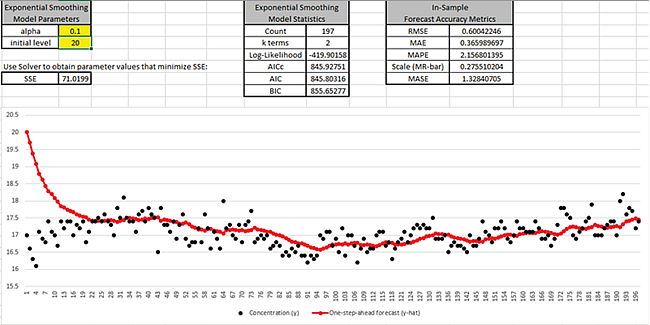

Enter alpha = 0.1 and initial level = 20 as shown:

This initial level is a poor estimate of the start value and results in SSE = 71.02. After

about 30 observations, the influence of this poor start value is negligible.

The duration for which the initial level has influence on the one-step-ahead forecast

depends on alpha, a smaller alpha would be a longer duration; a larger alpha would be a

shorter duration.

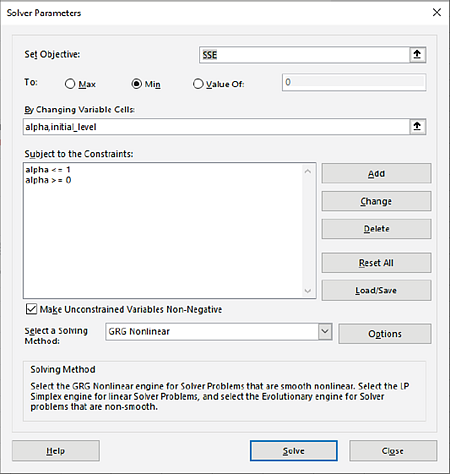

Now we will use Excels Solver to find the optimal values for alpha

and initial level. Click Data > Solver. (If the

Solver menu is not available, click

File > Options > Add-Ins. Click

Go Manage Excel Add-ins, check Solver Add-in. Click

OK. Click Data > Solver.)

The cell addresses, constraints and settings for Solver have been stored in the workbook, so

no changes are necessary. Solver will minimize cell G7 (SSE), by varying

cells G3 (alpha) and G4 (initial_level).

The solving method is GRG Nonlinear; Evolutionary could also be used but it is

slower.

Click Solve. The Solver Results dialog shows that

a solution has been found.

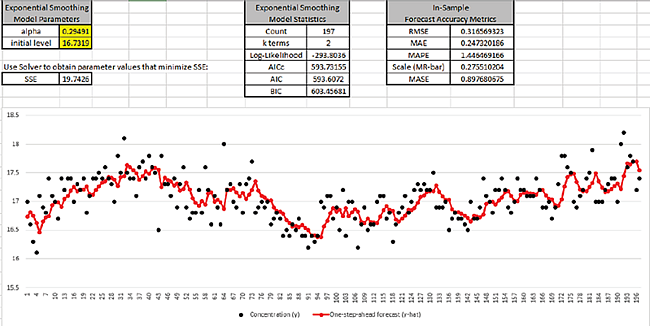

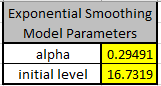

Click OK. The SSE is now 19.74; alpha value =

0.295 and initial level = 16.732.

By minimizing the residual sum-of-squares error (SSE), we have our best estimate of the

parameters to produce one-step-ahead forecast values.

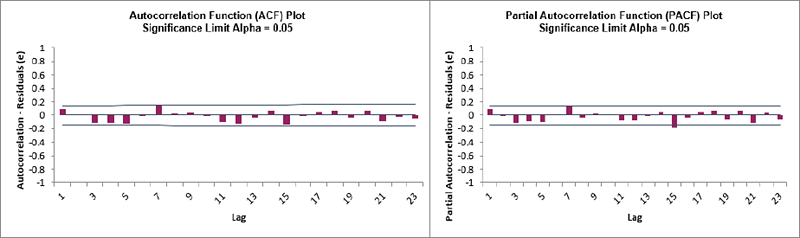

We will now produce ACF/PACF plots for the Residuals.

Select cells D1:D198 and click SigmaXL >

Time Series Forecasting > Autocorrelation (ACF/PACF)

Plots.

Click Next, Select Residuals (e), Click OK.

We can see that all of the autocorrelation has been removed by the simple exponential

smoothing model (with the exception of lag 15 in the PACF), so this is a good fit to the

time series data.

By way of comparison, these are the ACF/PACF plots for the original

Concentration data that we produced earlier.

We will now have a quick look at the Residuals using a Histogram.

Select the Residuals data (D1:D198). Click SigmaXL

> Graphical Tools > Histograms and Descriptive

Statistics. Next, Select Residuals (e), Click

OK.

The residuals are normally distributed with no obvious extreme outliers.

Chemical Process Concentration - Series A

Open Chemical Process Concentration Series A.xlsx

(Sheet 1 tab). This is the Series A data from

Box and Jenkins, a set of 197 concentration values from a

chemical process taken at two-hour intervals. See the Run Chart,

ACF/PACF Plots, Spectral.html and Seasonal Trend

Decomposition Plots for this data.

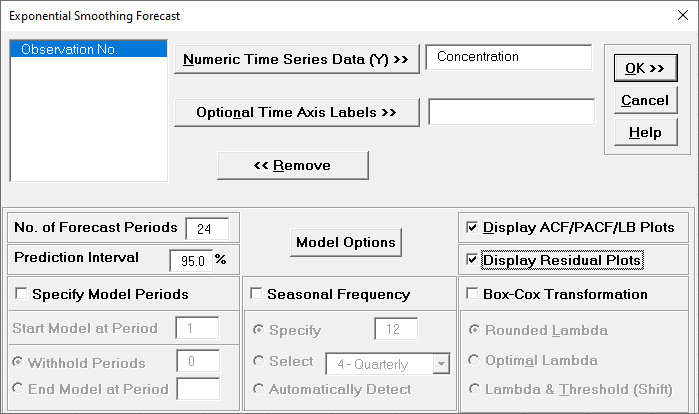

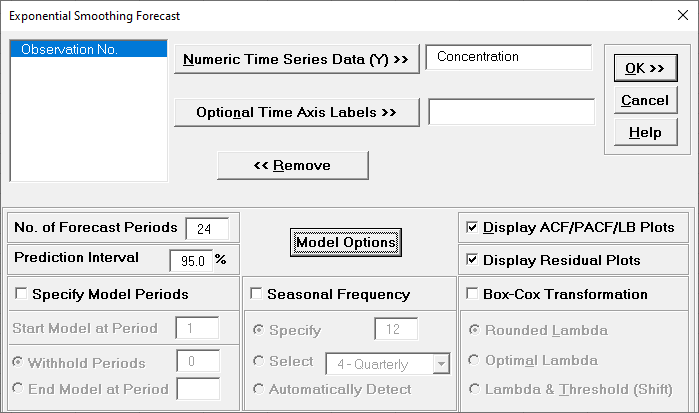

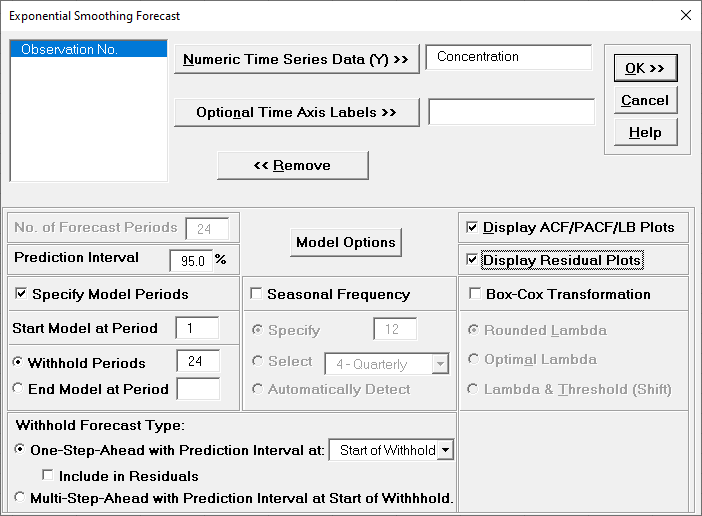

Click SigmaXL > Time Series

Forecasting > Exponential Smoothing Forecast > Forecast. Ensure that

the entire data table is selected. If not, check Use

Entire Data Table. Click Next.

Select Concentration, click

Numeric Data

Variable (Y) >>. Check Display

ACF/PACF/LB Plots and Display Residual Plots.

Leave Specify Model Periods, Seasonal Frequency

and Box-Cox Transformation unchecked. We will

use the default No. of Forecast Periods = 24

and Prediction Interval = 95.0 %.

Optional Time Axis Labels will be displayed on the forecast

chart time axis. If used, dates for the forecast periods should

also be included, otherwise the time axis will be blank for the

forecast periods.

No. of Forecast Periods are the number of time series values

to be predicted (forecast horizon). The most accurate forecast

will be for the first predicted value (one-step-ahead).

Prediction Interval % is the confidence level for the

individual predictions. For example, a 95% prediction interval

contains a range of values which should include the actual

future value with 95% probability. The interval will get larger

the further out you predict.

Model Options opens another dialog which allows you to set automatic

options or to specify a model.

Display ACF/PACF/LB option will produce ACF

and PACF plots for the raw data as well as for the model

residuals. The LB plot is a plot of Ljung-Box test P-Values for

various lags and is used to determine if a group of

autocorrelations are significant, (i.e., the autocorrelations do

not come from a white noise series).

Display Residual Plots will produce a table of model residuals and the

usual model residual plots: histogram, normal probability plot, residuals versus data order,

and residuals vs forecast value. Note that if a Box-Cox transformation is applied, the

residuals are transformed so will not be equal to forecast - actual.

Specify Model Periods are used to specify a start period, end period or

withhold sample. The withheld data is not used in model estimation, so this is very useful

for model validation and comparison. This will be used in a later example.

Seasonal Frequency and Box-Cox Transformation will be

used in a later example.

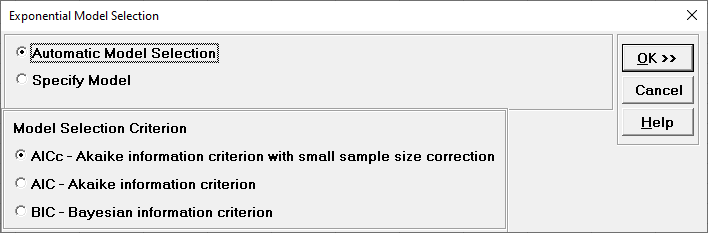

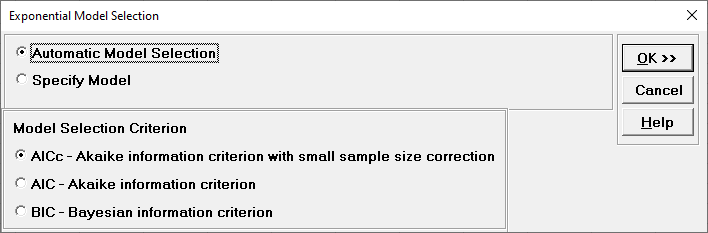

Click Model Options.

Automatic Model Selection will be used later. It is the default

selection.

Model Selection Criterion is the information criterion metric to be used

in automatic model selection. AICc is the default selection.

Clicking OK accepts the settings and returns you to the previous dialog.

Clicking

Cancel will cancel any changes and return you to the previous dialog.

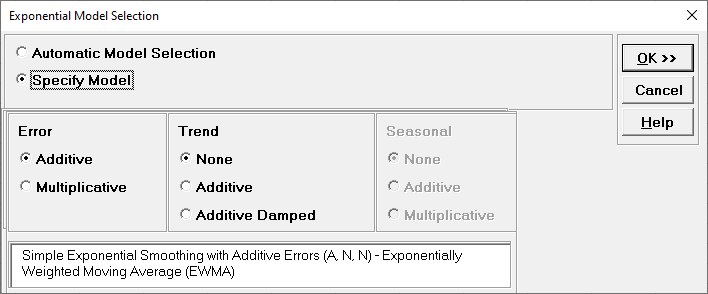

Select Specify Model.

Specify Model allows you to manually specify

the Error-Trend-Seasonal model. Seasonal options are greyed out

because the Seasonal Frequency option in the

main dialog is unchecked. A summary description of the model is

also given. This will be included in the forecast report.

We will use the default Error:

Additive and Trend: None, which is a

simple exponential smoothing model, the same as was demonstrated

previously. Click OK to return to the

Exponential Smoothing Forecast dialog. Click OK.

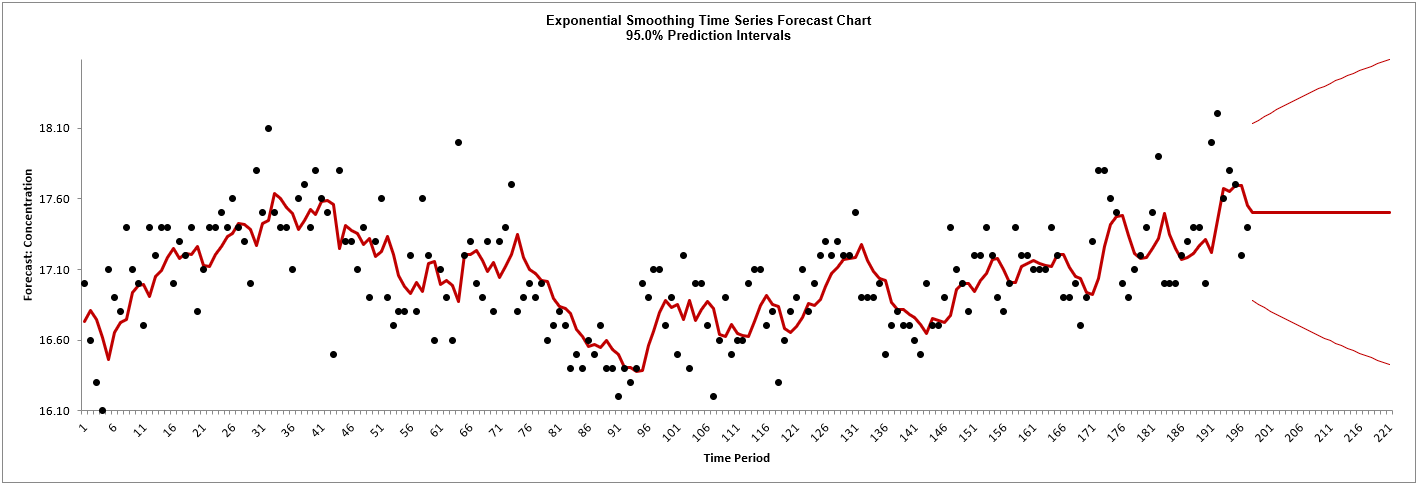

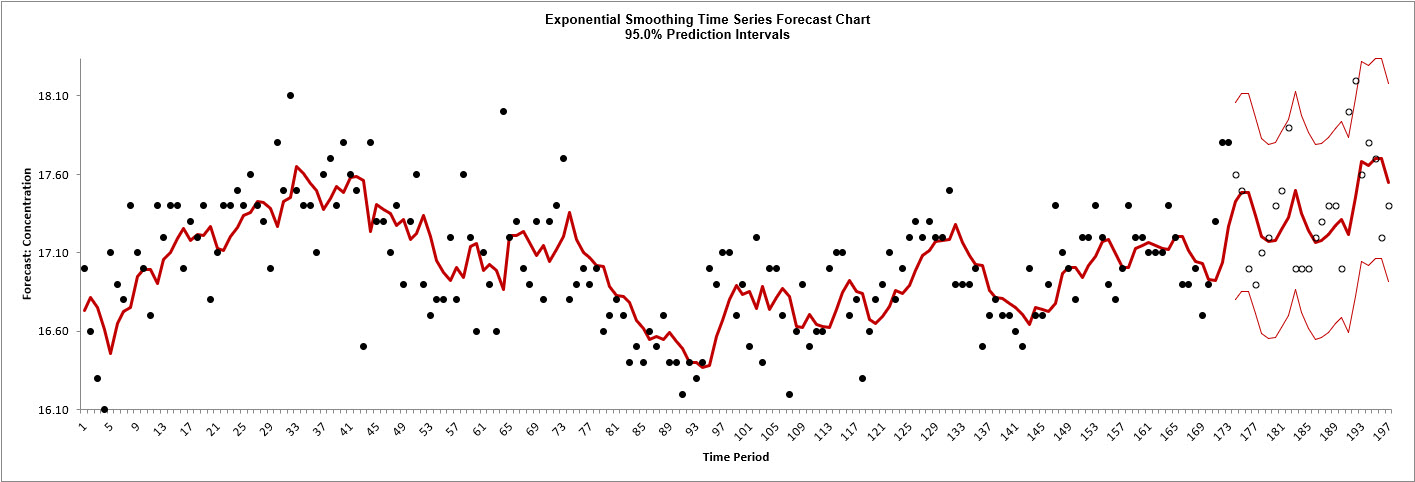

The exponential smoothing forecast chart is given:

This is very similar to the exponential smooth plot demonstrated

above, showing the raw Concentration data (black) and

one-step-ahead forecast values (red), but with the addition of a

24-period forecast and the 95% prediction interval.

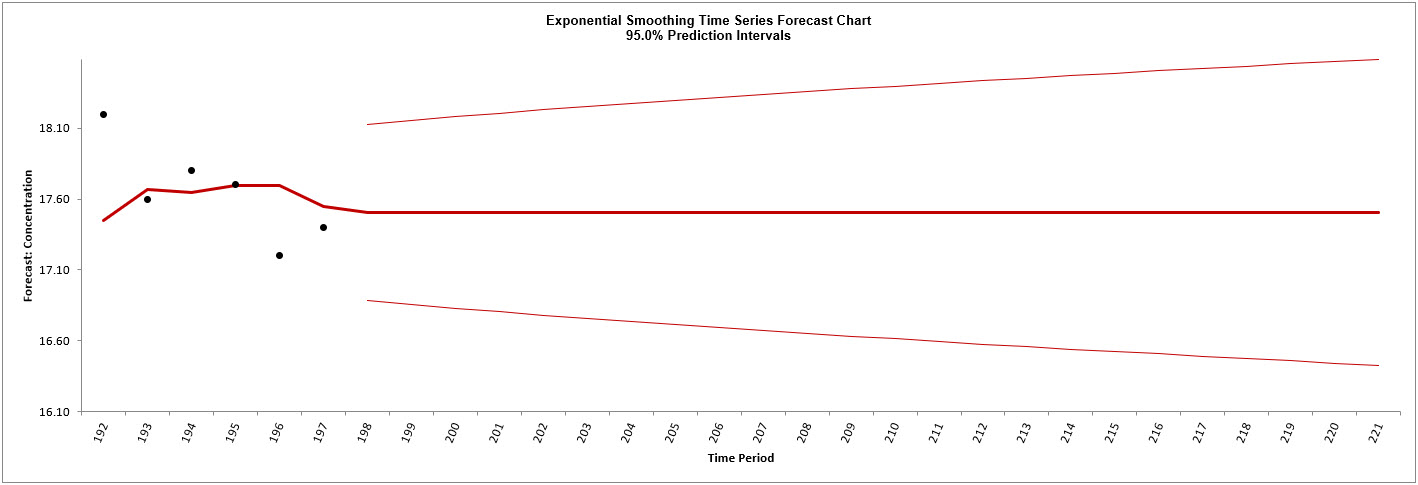

You can zoom in to view the last 30

points on the Forecast Chart. Click SigmaXL Chart Tools

> Show Last 30 Data Points.

To restore the chart, click

SigmaXL Chart Tools > Show All Data Points.

You can also scroll through the data.

Click SigmaXL Chart Tools > Enable Scrolling

You are prompted with a warning message that custom formatting

on the chart will be cleared:

You can avoid seeing this warning by checking Save this

choice as default and do not show this form again.

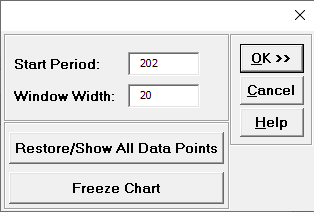

Click OK. The scroll

dialog appears allowing you to specify the Start Period

and Window Width:

At any point, you can click Restore/Show All Data Points

or Freeze Chart. Freezing the chart will remove

the scroll and unload the dialog. The scroll dialog will also

unload if you change worksheets. To restore the dialog, click

SigmaXL Chart Tools > Enable Scrolling.

Click OK. A scroll bar

appears beneath the forecast chart. You can also change the

Start Subgroup and Window Width

and Update.

You can scroll through by clicking to the right or left, with

the specified window width of 20. Click left once to view the

chart as shown.

Click Cancel to exit

the scroll dialog.

Scroll down to view the Exponential

Smoothing Model header:

The model Simple Exponential Smoothing with Additive Errors (A,

N, N) Exponentially Weighted Moving Average (EWMA) is the user

specified model. This is the same model information that was

displayed in the Model Selection dialog.

If we had checked Specify Model Periods in the main dialog, the

start, end or withhold selection would be summarized here as

well.

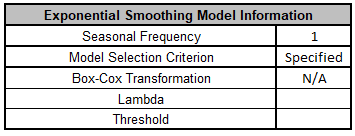

The Exponential Smoothing Model

Information is given as:

This is a summary of model information with Seasonal Frequency =

1 (nonseasonal); Model Selection Criterion = Specified because

the model was user specified; and Box-Cox Transformation = N/A

because Box-Cox Transformation was unchecked.

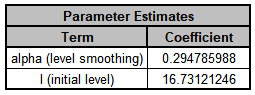

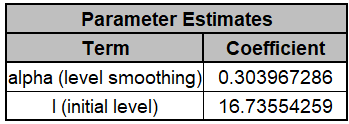

The Parameter Estimates are:

The parameter estimates closely match the values obtained

earlier in the demonstration using Solver:

The slight differences in parameter results are due to

differences in optimization method.

The results match those given in the demonstration using Solver:

The equations may be viewed by clicking on the Demo

cells

M5, M6, M7 or M8.

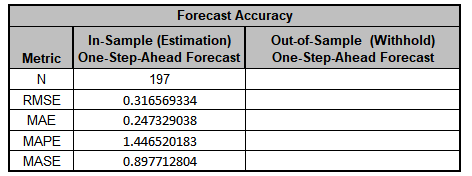

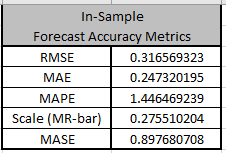

The In-Sample Forecast Accuracy metrics

are:

MASE is less than one, so it is a better forecast than would be

obtained from a nave forecast (set all forecasts to be the

value of the last observation). See Forecast Accuracy Metrics.

The results closely match those given in the demonstration using

Solver:

The equations may be viewed by clicking on the Demo

cells

P3 to P7.

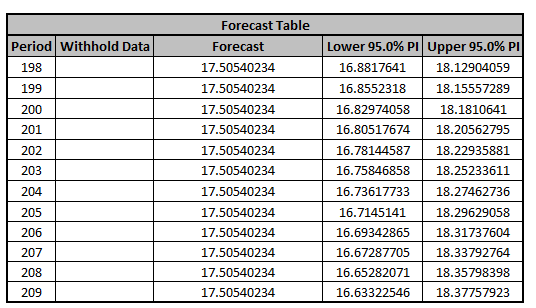

The Forecast Table is given as:

These are the same forecast and prediction interval

values displayed in the Forecast Chart but provided for further analysis or charting. If

Withhold Periods are specified, the Withhold Data will be displayed as well.

Click on the Exp. Smooth. ACF

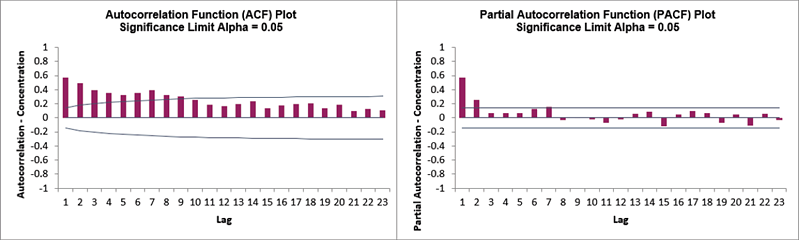

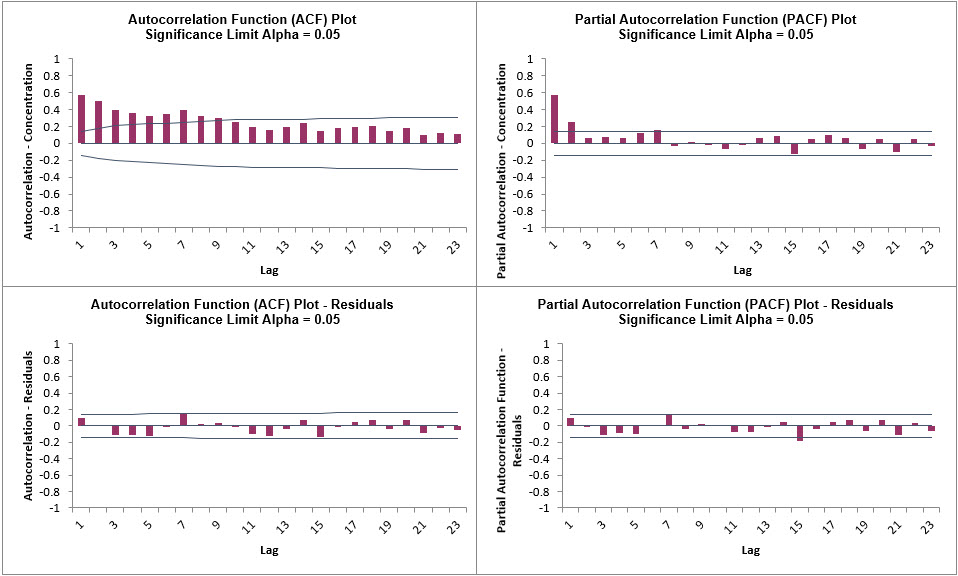

PACF LB sheet to view the ACF/PACF/LB Plots:

These match the plots that we obtained previously in the Demo.

We can see that all of the autocorrelation has been removed by

the exponential smoothing model (with the exception of lag 15 in

the PACF), so this is a good fit to the time series data.

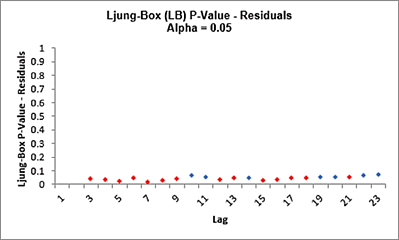

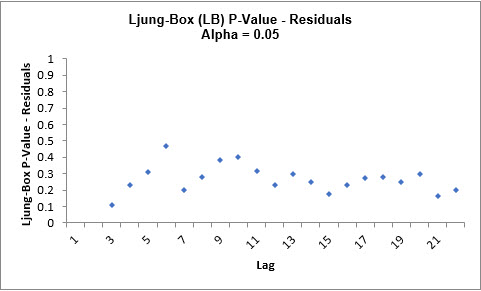

The LB plot is a plot of Ljung-Box test P-Values for various lags and is used to

determine if a group of autocorrelations are significant, (i.e., the autocorrelations do

not come from a white noise series).

For further details, see Ljung-Box Test.

The red P-Values are significant (alpha=.05) and the blue P-Values are not significant.

It is desirable that all P-Values be blue. The ACF/PACF plots indicated that almost all

of the correlation has been accounted for in the model, but the Ljung-Box plot shows

that some significant autocorrelation still remains - so the model can potentially be

improved. This does not mean that the model is a bad model, it can still be very useful

for prediction purposes, but the prediction intervals may not provide accurate

coverage.

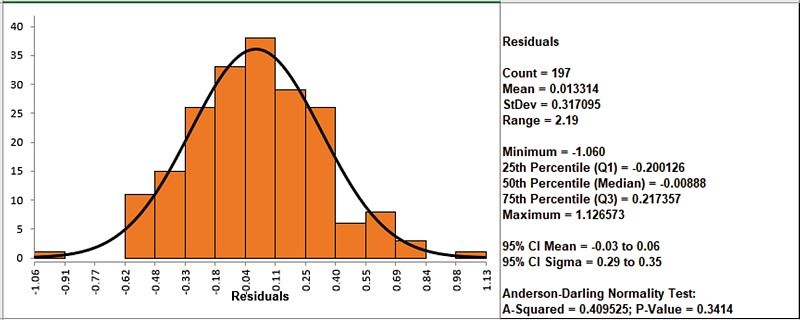

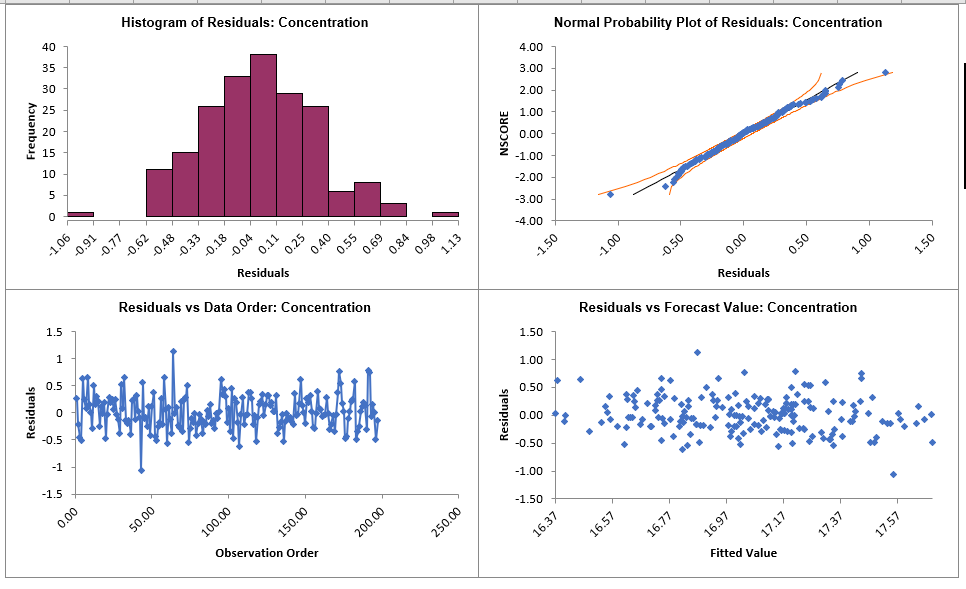

Click on the Exp. Smoothing Residuals

sheet to view the Residual Plots:

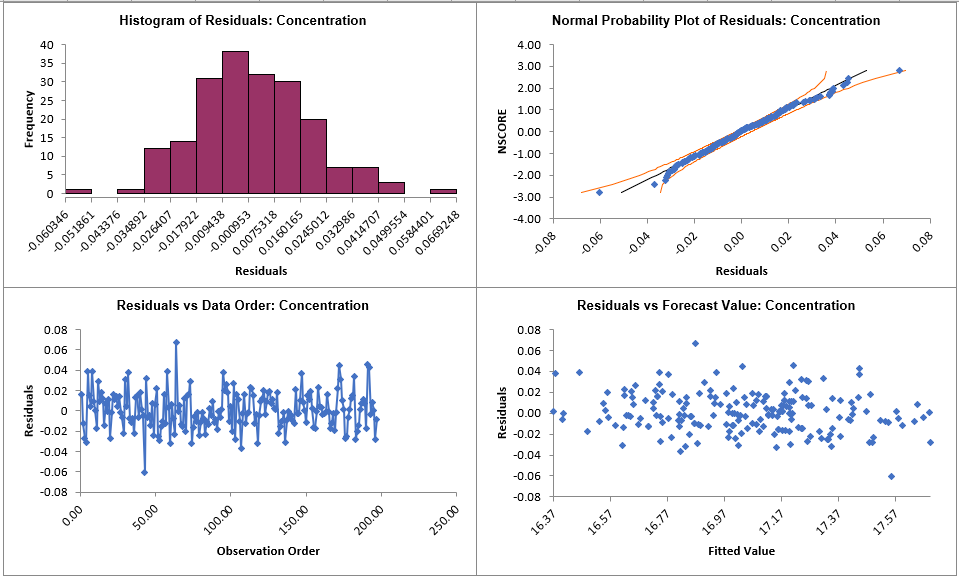

These residual plots are the same as used in SigmaXLs Multiple

Regression. The histogram matches what we obtained in the Demo

(the normal curve is not applied here). The residuals are

approximately normally distributed, with a roughly straight line

on the normal probability plot. There are no obvious extreme

outliers or patterns in the charts. Later, we will apply a

control chart to the residuals to formally test for significant

outliers or assignable causes.

Now we will rerun Exponential Smoothing

on the Concentration data but use Automatic Model Selection.

Click Recall SigmaXL Dialog menu or press

F3 to

Recall Last Dialog.

Click Model Options.

Select Automatic Model Selection. We will use

the default Model Selection Criterion: AICc Akaike

information criterion with small sample size correction.

Click OK to return to

the Exponential Smoothing Forecast dialog. Click OK. The

exponential smoothing forecast report is given.

Scroll down to view the Exponential

Smoothing Model header:

The model Simple Exponential Smoothing with

Multiplicative Errors (M, N, N) was selected as the

best fit for the Concentration data based on the AICc criterion.

The point forecasts produced by the Multiplicative and Additive

models are identical if they use the same smoothing parameter

values. Multiplicative will, however, generate different

prediction intervals to accommodate change in variance.

The Exponential Smoothing Model

Information is given as:

This is a summary of model information with Seasonal

Frequency = 1 (nonseasonal); Model Selection Criterion = AICc and Box-Cox

Transformation = N/A because Box-Cox Transformation was unchecked.

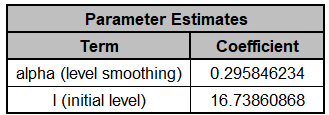

The Parameter Estimates are:

These are fairly close to the parameter estimates

obtained above using the additive model.

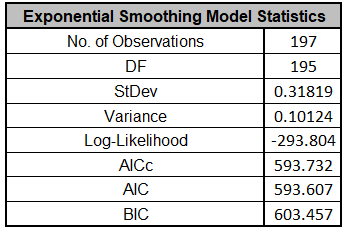

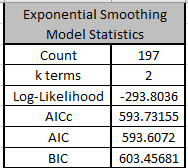

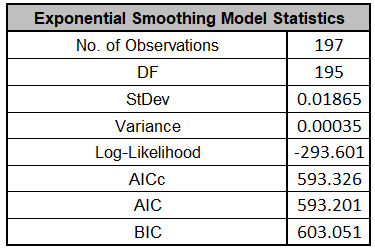

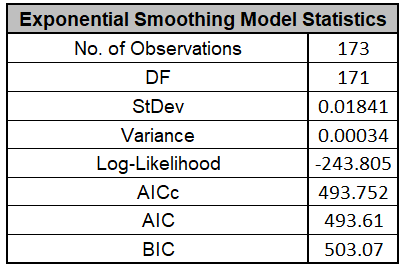

The Exponential Smoothing Model Statistics are:

The Log-Likelihood, AICc, AIC and BIC are close to the

values obtained above

using the additive model, but the Log-Likelihood is slightly

higher giving a lower AICc, so multiplicative was selected as

the best model. Note however that the StDev and Variance are

very different. This difference is due to the multiplicative

residuals being relative errors:

The In-Sample Forecast Accuracy metrics, Forecast Table and

ACF/PACF/LB Plots for multiplicative are very close to the

additive model. The multiplicative residual plots look the same,

but note the different scale due to the relative errors.

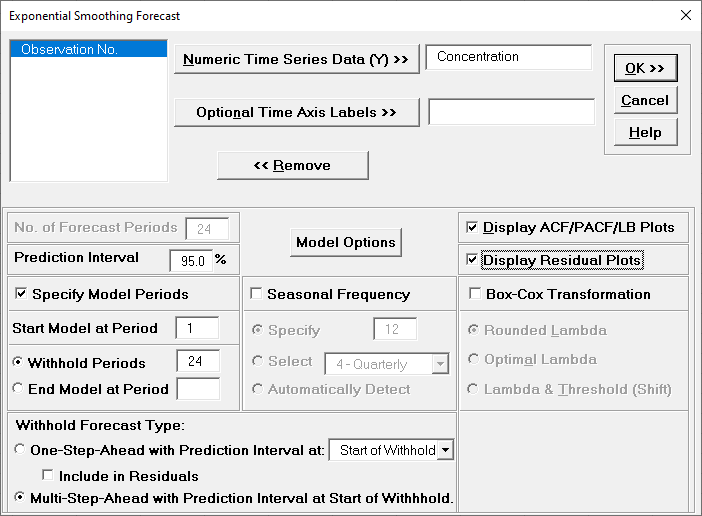

Now we will rerun Exponential Smoothing on the Concentration

data with Automatic Model Selection, but will use Specify

Withhold Periods. Click Recall SigmaXL Dialog menu or press F3

to Recall Last Dialog. Check Specify Model Periods. Set Withhold

Periods = 24 (i.e., we will forecast 24 periods and compare

against the withheld actual). We will use the default Withhold

Forecast Type: One-Step-Ahead with Prediction Interval at:Start

of Withhold.

Specify Model Periods option allows you to specify the start and end

periods used in automatic model identification and parameter estimation. Typically,

Start Model at Period is kept = 1 and Withhold Periods specifies the

number of periods to be withheld for out-of-sample testing.

End Model at Period specifies the end period, so the withhold sample

size would be: total number of observations end period.

Withhold Forecast Type: One-Step-Ahead will exclude the withhold

sample from automatic model identification and parameter estimation, but uses the

withhold data to update the predicted one-step ahead forecast. This is useful to assess

forecast error when you only care about the short-term one-step ahead

prediction.

Withhold Forecast Type: One-Step-Ahead with Prediction Interval at:

Start of Withhold will display the prediction interval for the duration of the

withhold sample. Note that the length of the prediction interval is determined by the

number of withhold periods, so overrides the specified

No. of Forecast Periods.

Withhold Forecast Type: One-Step-Ahead with Prediction Interval at:

End of Withhold will display the prediction interval at the end of the withhold

sample. The length of the prediction interval is determined by the specified

No. of Forecast Periods.

Include in Residuals will treat the one-step-ahead forecast errors as

residuals (even though they were not part of the model estimation process) and will be

included in the ACF/PACF/LB Residual Plots along with the Residuals report and graphs.

Typically, this is kept unchecked.

Withhold Forecast Type: Multi-Step-Ahead with Prediction Interval at Start of

Withhold will exclude the withhold sample from automatic model

identification and parameter estimation and does not use the withhold data to update the

predicted one-step ahead forecast. This is useful to assess forecast error when you are

interested in a long-term forecast window (horizon). The prediction interval will be

displayed for the duration of the withhold sample. Note that the length of the

prediction interval is determined by the number of withhold periods, so overrides the

specified

No. of Forecast Periods. These forecast errors are not included in

ACF/PACF/LB Residual Plots or the Residuals report and graphs.

Click Model Options. Select Automatic Model Selection.

We will

use the default Model Selection Criterion: AICc Akaike

information criterion with small sample size correction.

Tip: When using Recall SigmaXL Dialog, and if there

are no changes to the

Model Option settings, the previous settings will be used. It is not

necessary to repeat this step.

Click OK to return to the Exponential Smoothing

Forecast dialog. Click OK. The exponential

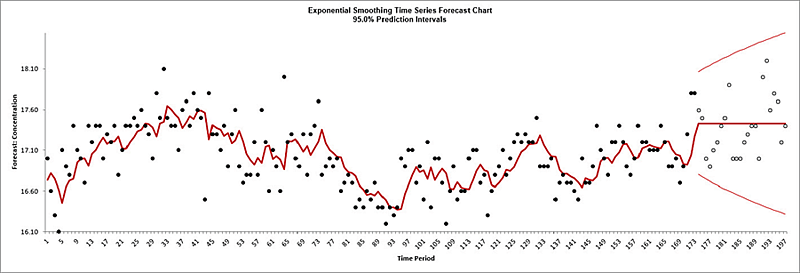

smoothing forecast report is given:

The blank dots are the data values in the withhold

sample with a one-step-ahead forecast and prediction intervals displayed at the start of

the withhold sample.

Scroll down to view the Exponential Smoothing Model header:

As with the complete data, the model

Simple Exponential Smoothing with Multiplicative Errors (M, N, N) was

selected as the best fit for the Concentration data based on the AICc criterion. The

header also includes the number of specified withhold periods.

The Parameter Estimates are:

These are close to the parameter estimates obtained above (which

used all of the data with the multiplicative model).

The Exponential Smoothing Model Statistics are:

These are fairly close to the model statistics obtained above (which

used all of the data with the multiplicative model). Here we are using only 173 of the

197 observations.

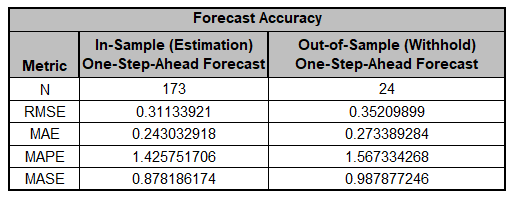

The Forecast Accuracy metrics are:

As expected, the

Out-of-Sample (Withhold) One-Step-Ahead Forecast errors are larger than

the

In-Sample (Estimation) One-Step-Ahead Forecast errors.

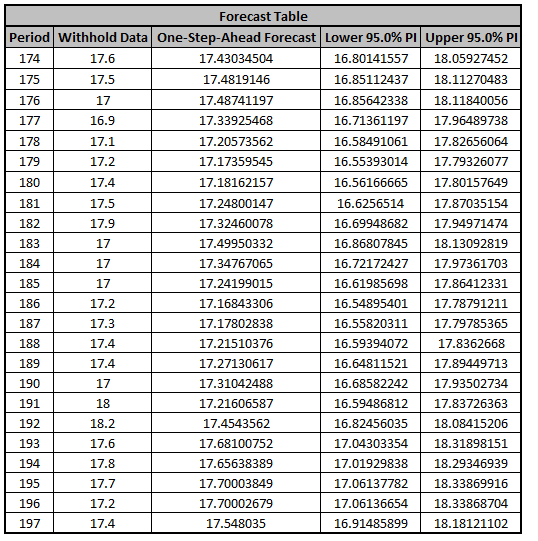

The Forecast Table is given as:

These are the same forecast and prediction interval

values displayed in the Forecast Chart, but provided for further analysis or charting.

The

Withhold Data is also displayed.

The ACF/PACF/LB Residual Plots and Residual Plots are based on

the in-sample data. The plots look similar to the complete data

above, except for the Ljung-Box P-Values:

The

Simple Exponential Smoothing with Multiplicative Errors (M, N, N) model

is a better fit to the subset than the complete data, with all P-Values being blue (>

.05).The

Simple Exponential Smoothing with Multiplicative Errors (M, N,

N) model is a better fit to the subset than the complete data,

with all P-Values being blue (> .05).

If Include in Residuals was checked then the

residuals would also include the Out-of-Sample

(Withhold) One-Step-Ahead Forecast errors.

Now we will rerun Exponential Smoothing on the Concentration

data, but use Multi-Step-Ahead for the Withhold Forecast. Click

Recall SigmaXL Dialog menu or press F3 to recall last

dialog.

Select Withhold Forecast Type: Multi-Step-Ahead with Prediction

Interval at Start of Withhold.

Click OK. The exponential smoothing forecast

report is given:

The blank dots are the data values in the withhold sample with a multi-step forecast

and prediction intervals displayed at the start of the withhold sample.

The Forecast Accuracy metrics are:

As expected, the

Out-of-Sample (Withhold) Multi-Step-Ahead Forecast errors are larger

than the

In-Sample (Estimation) One-Step-Ahead Forecast errors and the

Out-of-Sample (Withhold) One-Step-Ahead Forecast errors above.

Monthly Airline Passengers - Series G

Open Monthly Airline Passengers - Series G.xlsx (Sheet 1 tab). This is the Series G data from Box and Jenkins, monthly total international airline passengers for January 1949 to December 1960.

See the Run Chart, ACF/PACF Plots, Spectral.html and Seasonal Trend Decomposition Plots for this data.

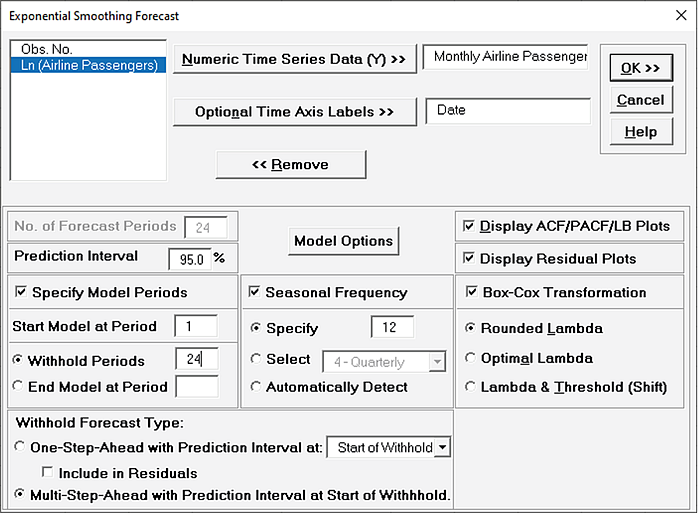

Click SigmaXL > Time Series Forecasting > Exponential Smoothing Forecast > Forecast. Ensure that the entire data table is selected. If not, check Use Entire Data Table. Click Next.

Select Monthly Airline Passengers, click Numeric Time Series Data (Y) >>.

Select Date, click Optional Time Axis Labels >>.

Check Display ACF/PACF/LB Plots and Display Residual Plots. Check Specify Model Periods.

Set Withhold Periods = 24 (i.e., we will forecast 24 months and compare to withheld actual).

Select Withhold Forecast Type: Multi-Step-Ahead with Prediction Interval at Start of Withhold.

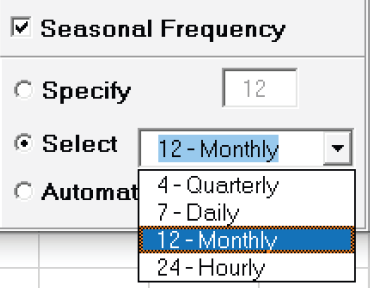

Check Seasonal Frequency with Specify = 12.

Check Box-Cox Transformation and select Rounded Lambda (selected because the Run Chart showed an increase in the seasonal variance over time).

We will use the default Prediction Interval = 95.0%.

Withhold Forecast Type: Multi-Step-Ahead with Prediction Interval at Start of Withhold will exclude the withhold sample from automatic model identification and parameter estimation and does not use the withhold data to update the predicted one-step ahead forecast.

This is useful to assess forecast error when you are interested in a long-term forecast window (horizon).

The prediction interval will be displayed for the duration of the withhold sample.

Note that the length of the prediction interval is determined by the number of withhold periods, so overrides the specified

No. of Forecast Periods.

Seasonal Frequency Specify is used to specify the seasonal frequency.

Note that Exponential Smoothing is limited to a maximum seasonal frequency of 24. For higher frequencies use Exponential Smoothing Multiple Seasonal Decomposition (MSD)

Seasonal Frequency Select gives a drop-down list of commonly used seasonal frequencies:

Seasonal Frequency Automatically Detect should be used if uncertain what the seasonal frequency value is (or do a Spectral.html prior to the Seasonal Trend Decomposition Plots). If detected frequency is > 24, 1 is returned.

If that occurs, please use Exponential Smoothing Multiple Seasonal Decomposition (MSD).

Box-Cox Transformation with Rounded Lambda will select Lambda = 0 (Ln), 0.5 (SQRT) or 1 (Untransformed).

Threshold (Shift) is computed automatically if the time series data includes 0 or negative values, otherwise it is 0.

Box-Cox Transformation with Optimal Lambda uses the range of 0 to 1 for Lambda.

Threshold is computed automatically if the time series data includes 0 or negative values.

Box-Cox Transformation with Lambda & Threshold (Shift) if left blank, will compute optimal lambda and threshold.

The user may also specify Lambda and Threshold.

Lambda may be specified outside of the 0 to 1 range, but practically for time series analysis, should be limited to -1 to 2.

Threshold is typically 0, but if the time series data includes 0 or negative values, a negative threshold value should be entered that is smaller than the minimum data value.

This value will be subtracted from the data resulting in positive time series values.

Click Model Options.

We will use the default Automatic Model Selection with AICc as the Model Selection Criterion.

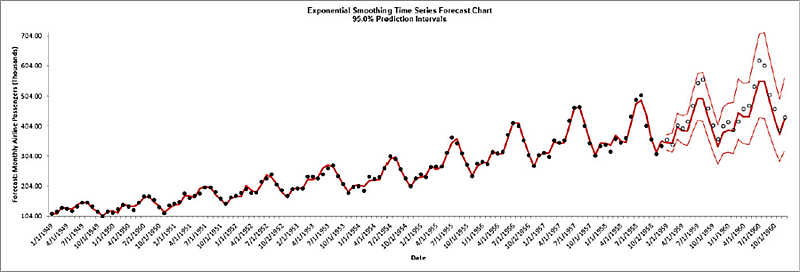

Click OK to return to the Exponential Smoothing Forecast dialog. Click OK. The exponential smoothing forecast report is given:

The blank dots are the data values in the withhold sample with a multi-step forecast and prediction intervals displayed at the start of the withhold sample.

Note that the data has been transformed using Box-Cox, but the inverse transformation is applied to produce this chart with the original units.

Scroll down to view the Exponential Smoothing Model header:

The model Additive Trend,

Additive Seasonal Method with Additive Errors (Holt-Winters) (A, A, A) was automatically selected as the best fit for the Box-Cox transformed Airline Passenger data based on the AICc criterion. Note that multiplicative models are not considered when

Box-Cox Transformation is checked. If a multiplicative model was desired, then one could manually transform the data and model Ln(Airline Passengers) with

Box-Cox Transformation unchecked.

The header also includes the number of specified withhold periods.

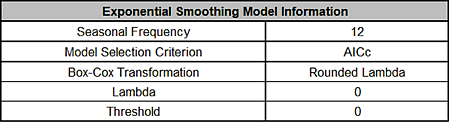

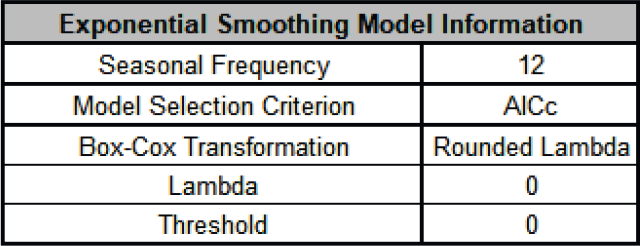

The Exponential Smoothing Model Information is given as:

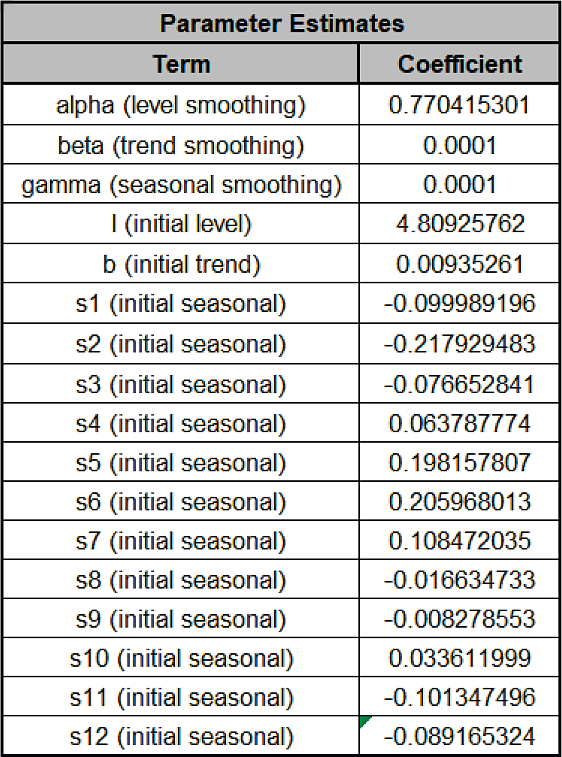

The Parameter Estimates are:

Error includes the smoothing parameter alpha and initial level value (l). The error is additive, but on the Ln transformed data.

Trend adds a smoothing parameter (beta) and initial trend value (b).

Seasonal adds a smoothing parameter (gamma) and initial seasonal values (s1 to s12), constrained to sum to zero for additive.

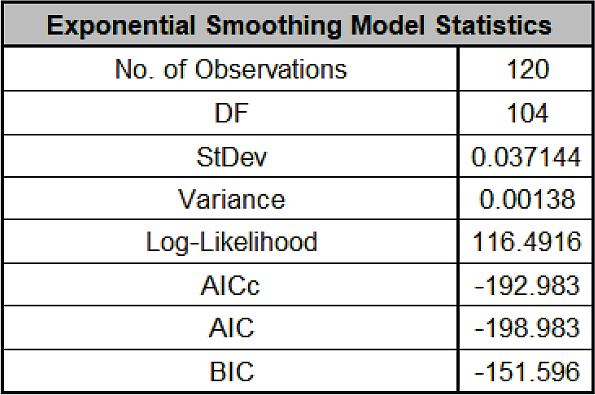

The Exponential Smoothing Model Statistics are:

The number of observations, n = 144 24 (withhold) = 120

Degrees of freedom (DF) = 120 (n) 16 (terms in the model, excluding s12) = 104

Note that the model statistics are based on the Ln transformed data, not the original data.

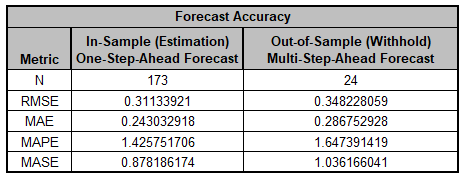

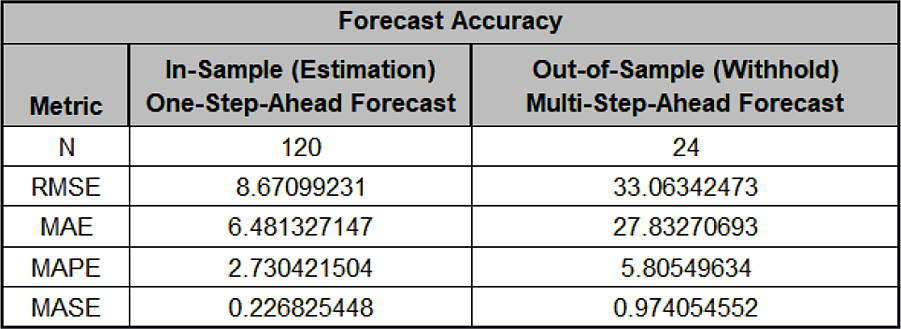

The Forecast Accuracy metrics are:

As expected, the Out-of-Sample (Withhold) Multi-Step-Ahead Forecast errors are larger than the In-Sample (Estimation) One-Step-Ahead Forecast errors.

Note, if we were primarily interested in a short term one-step ahead forecast, then we would have selected Withhold Forecast Type: One-Step-Ahead and this table would show Out-of-Sample (Withhold) One-Step-Ahead Forecast errors.

Forecast Accuracy metrics are calculated using the actual raw data versus inverse transformed forecast as displayed in the Forecast Chart and Table, so allows comparison across all model types and transformations.

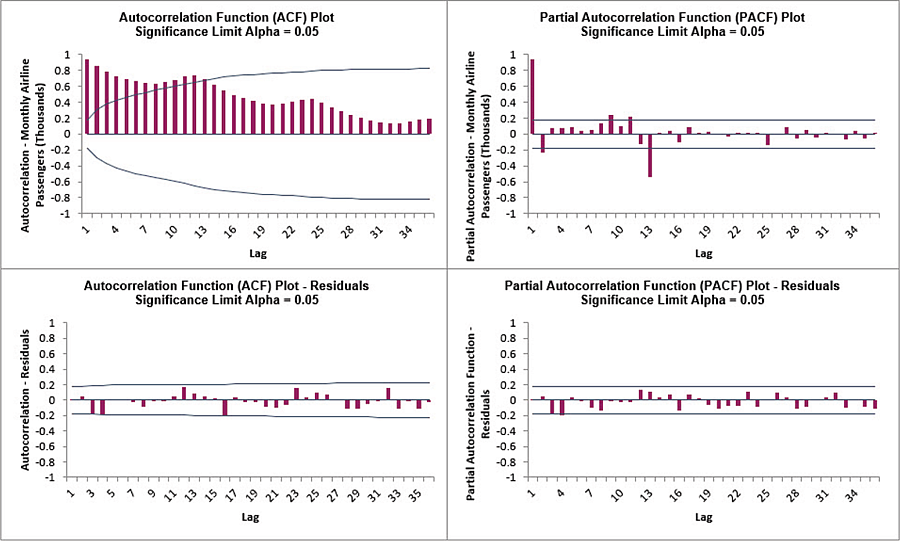

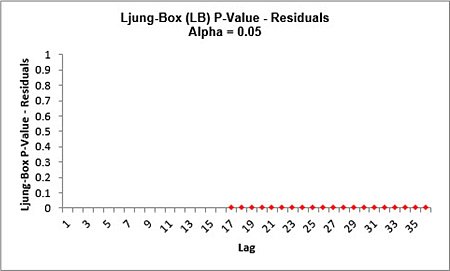

Click on the Exp. Smooth. ACF PACF LB sheet to view the ACF/PACF/LB Plots:

The ACF/PACF Residuals Plots indicate that almost all of the autocorrelation has been accounted for in the model, but the Ljung-Box plot shows that significant autocorrelation still remains (the red P-Values are significant at alpha=.05) - so the model can potentially be improved.

This does not mean that the model is a bad model, it can still be very useful for prediction purposes, but the prediction intervals may not provide accurate coverage.

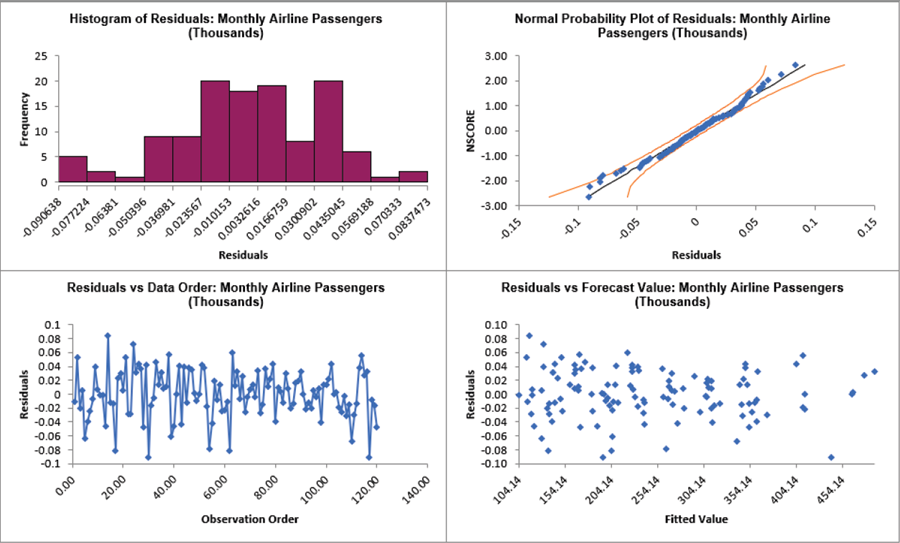

Click on the Exp. Smoothing Residuals sheet to view the Residual Plots:

The residuals are approximately normally distributed, with a roughly straight line on the normal probability plot.

There are no obvious extreme outliers or patterns in the charts.

Note that the residuals are based on the Ln transformed data, not the original data.

The Exponential Smoothing Model Information to the right of the plots shows the Box-Cox Transformation information.