Open Chemical Process Concentration Series A.xlsx (Sheet 1 tab). This

is the Series A data from Box and Jenkins, a set of 197 concentration values from a

chemical process taken at two-hour intervals.

Click

SigmaXL > Time Series Forecasting > Seasonal Trend Decomposition

Plots. Ensure that the entire data table is selected. If not, Use

Entire Data Table. Click Next.

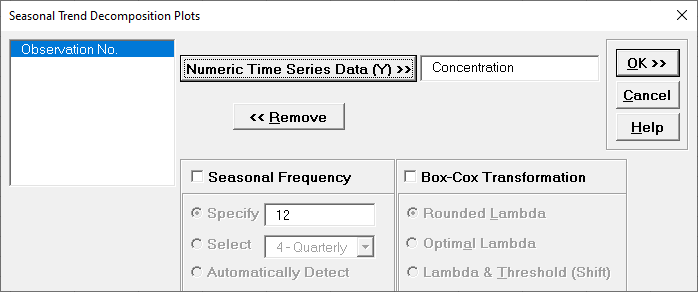

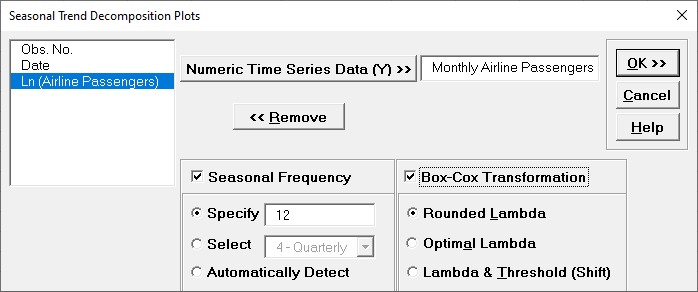

Click Concentration, click Numeric Time

Series Data (Y) >>. Seasonal Frequency and Box-Cox

Transformation should be unchecked as shown.

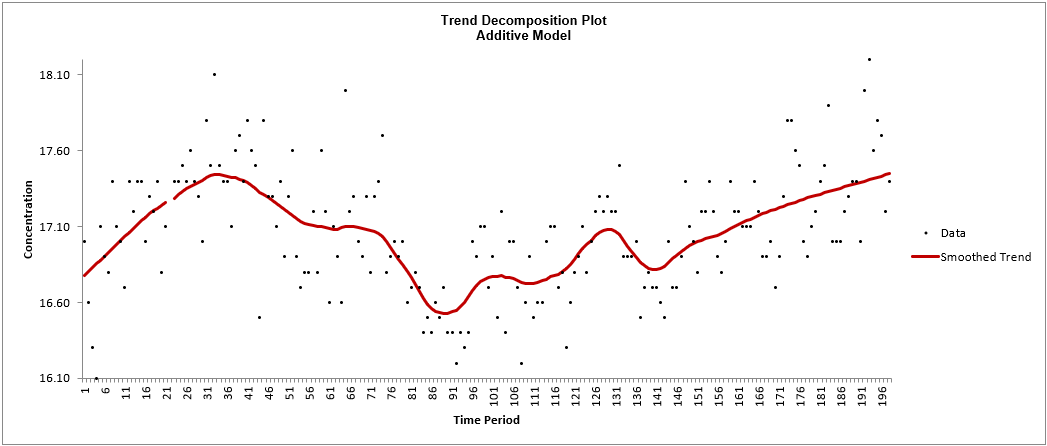

Click OK. A Trend Decomposition Plot for

Concentration is produced.

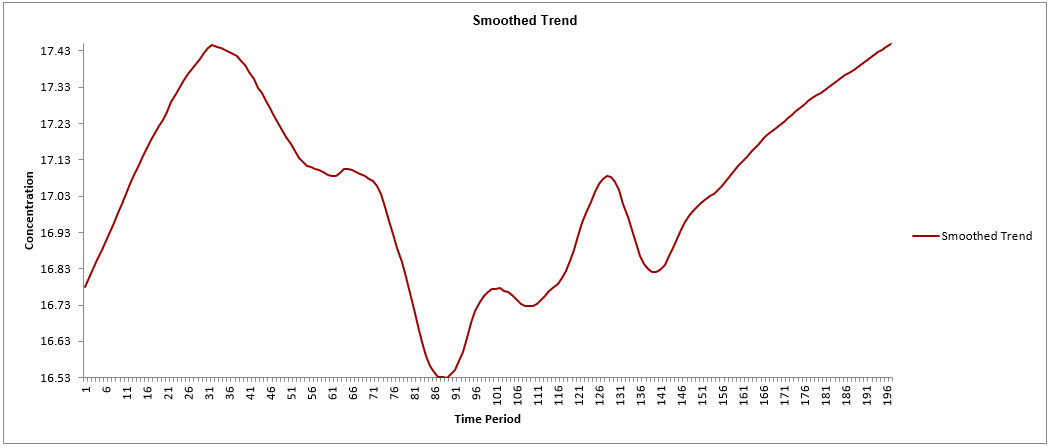

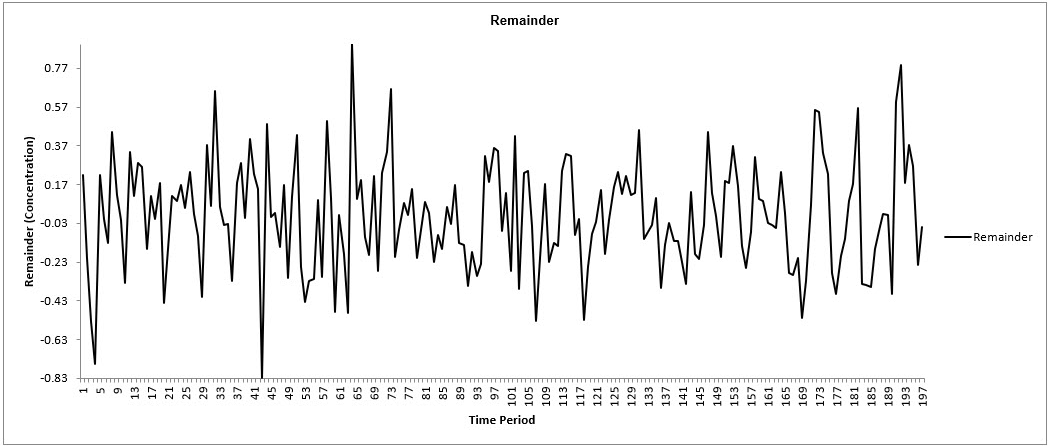

We can clearly see the wandering mean in this process. As discussed earlier, this can

be modeled with exponential smoothing or with ARIMA after differencing.

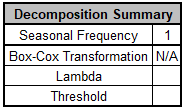

A Decomposition Summary report is also

included to the right of the plot, indicating seasonal frequency

and Box-Cox parameters (if applicable):

Seasonal Frequency = 1 denotes a nonseasonal process.

The Smoothed Trend and Remainder Plots are also produced as shown:

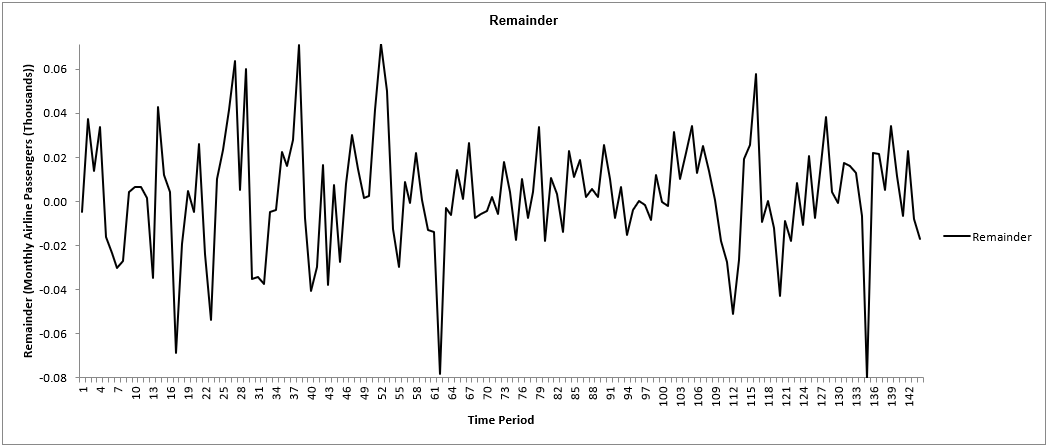

Monthly Airline Passengers - Series G

Open Monthly Airline Passengers - Series G.xlsx

(Sheet 1 tab). This is

the Series G data from Box and Jenkins, monthly total international airline passengers

for January 1949 to December 1960.

Click SigmaXL > Time Series Forecasting > Seasonal

Trend Decomposition Plots. Ensure that the entire data table is selected.

If not, check

Use Entire Data

Table. Click Next.

Select Monthly Airline Passengers, click Numeric

Time Series Data (Y). Check

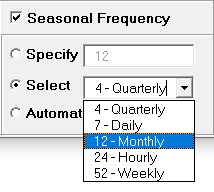

Seasonal Frequency with Specify = 12. Check

Box-Cox Transformation with Rounded Lambda (selected

because the Run Chart showed an increase in the seasonal variance over time).

Seasonal Frequency Specify also permits the entry of multiple

frequencies.

Seasonal Frequency Select gives a drop-down list of commonly used

seasonal frequencies:

Seasonal Frequency Automatically Detect should be used if uncertain

what the seasonal frequency value is (or do a Spectral.html prior to the

Seasonal Trend Decomposition Plots).

Box-Cox Transformation with Rounded Lambda will

select Lambda = 0 (Ln), 0.5 (SQRT) or 1 (Untransformed). Threshold (Shift) is computed

automatically if the time series data includes 0 or negative values, otherwise it is

0.

Box-Cox Transformation with Optimal Lambda uses the

range of 0 to 1 for Lambda. Threshold is computed automatically if the time series data

includes 0 or negative values.

Box-Cox Transformation with Lambda & Threshold

(Shift) if left blank, will compute optimal lambda and threshold. The user

may also specify Lambda and Threshold. Lambda may be specified outside of the 0 to 1

range, but practically for time series analysis, should be limited

to -1 to 2. Threshold is typically 0, but if the time series data includes 0 or negative

values, a negative threshold value should be entered that is smaller than the minimum

data value. This value will be subtracted from the data resulting in positive time

series values.

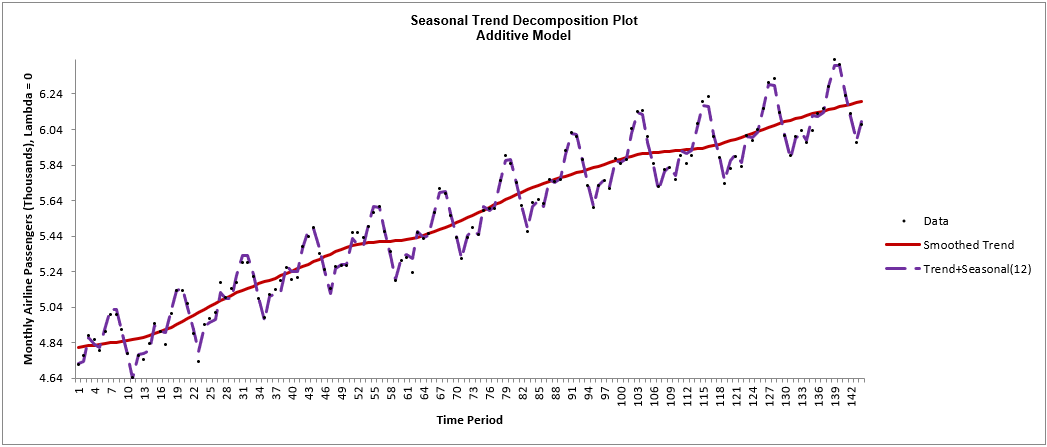

Click OK. A Seasonal Trend Decomposition Plot for Monthly Airline

Passengers is produced.

Here we see a strong positive trend as well as the monthly seasonal effect. Note that

this is the Lambda = 0 (Ln transformed) data. The Box-Cox transformation information is

given in the

Decomposition Summary report to the right of the plot:

Seasonal Frequency is 12 and Lambda = 0. The Ln transformed data are displayed to

maintain an additive model, which is easier to interpret than a multiplicative

model.

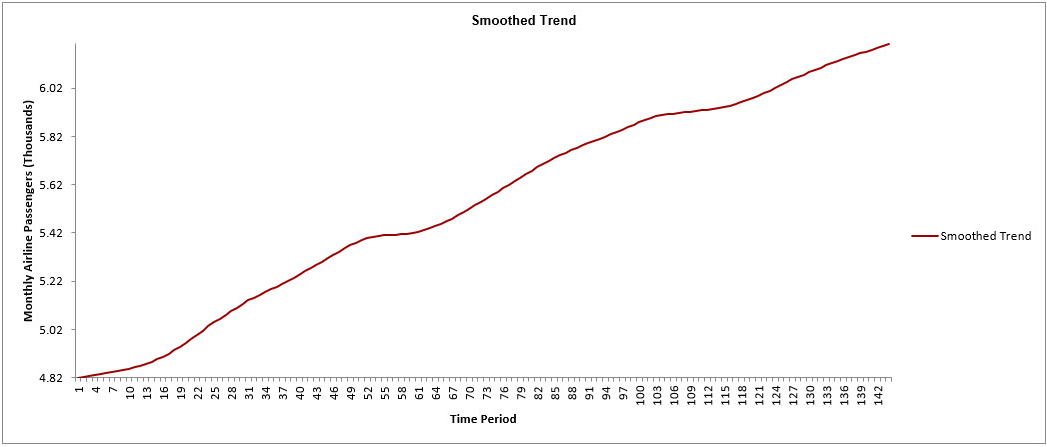

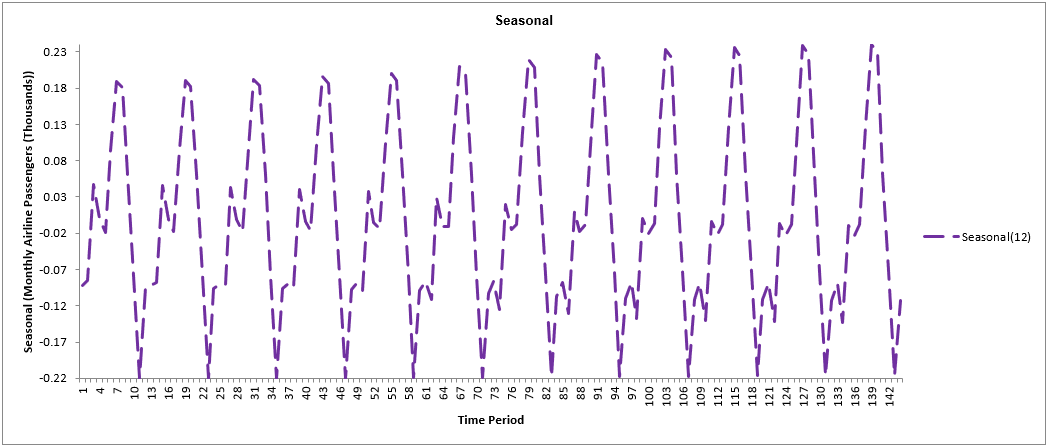

The Smoothed Trend, Seasonal and Remainder Plots are also produced

as shown:

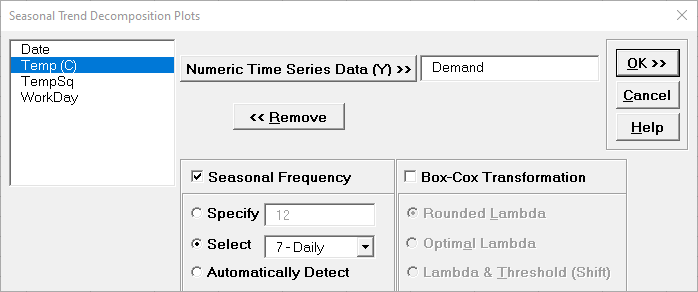

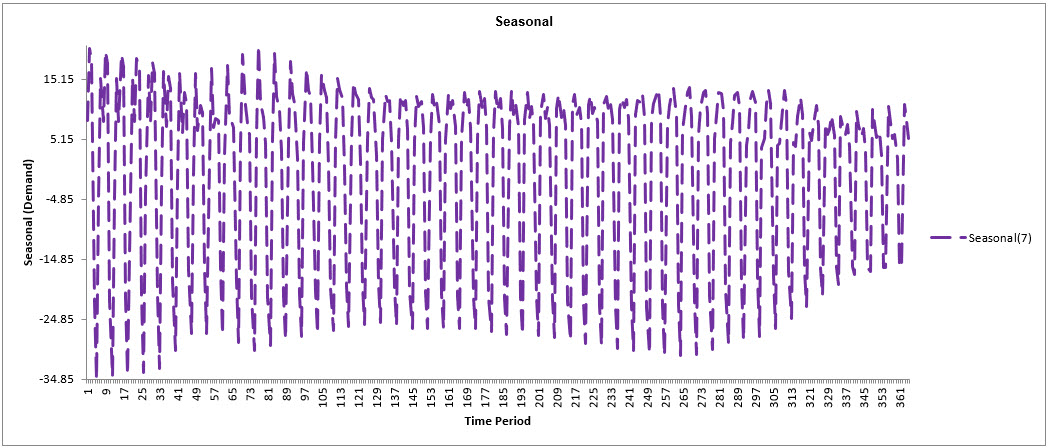

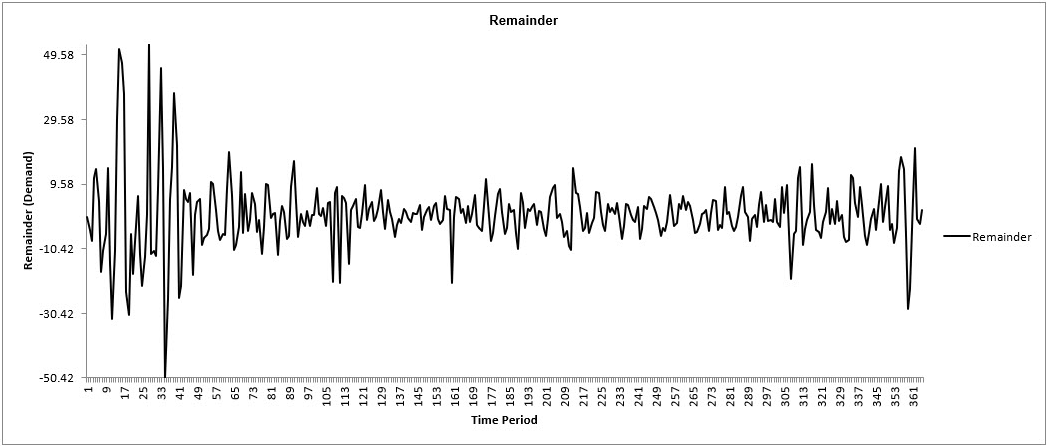

Daily Electricity Demand with Predictors ElecDaily

Open Daily Electricity Demand with Predictors

ElecDaily.xlsx (Sheet 1 tab). This is daily electricity

demand (GW) for the state of Victoria, Australia,

every day during 2014 (Hyndman, fpp2). This data has a seasonal frequency = 7

(observations per week).

Click SigmaXL > Time Series Forecasting > Seasonal

Trend Decomposition Plots. Ensure that the entire data table is selected.

If not, check

Use Entire Data Table. Click Next.

Select Demand, click Numeric Time Series Data (Y)

>>. Check

Seasonal Frequency with Select =

7-Daily selected from the drop-down list. Uncheck Box-Cox

Transformation.

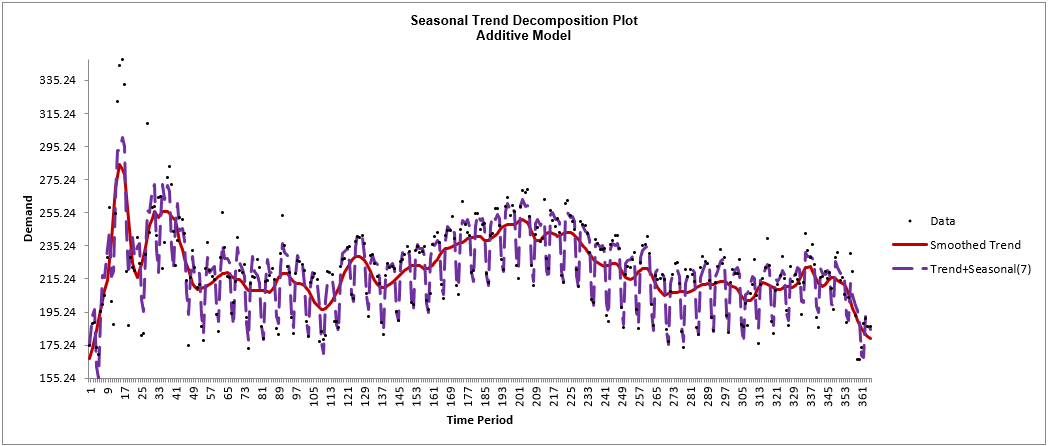

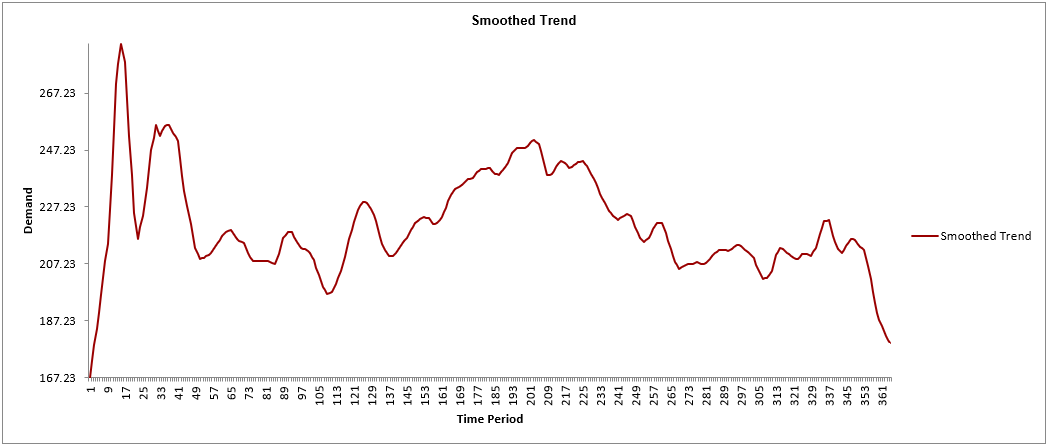

Click OK. A Seasonal Trend Decomposition Plot for

Demand is produced.

Here we see the daily seasonal effect. As discussed earlier, some of the trend patterns

can be explained by the predictors Temp (C), TempSq and WorkDay.

The Smoothed Trend, Seasonal and Remainder Plots are also produced

as shown:

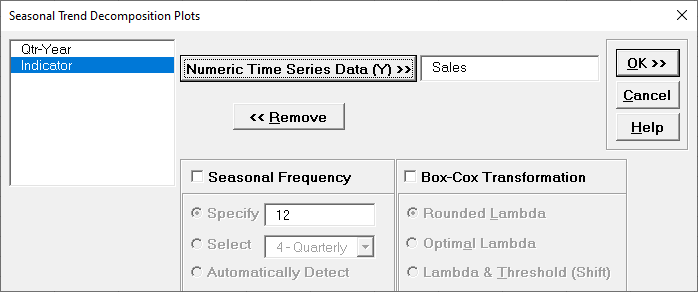

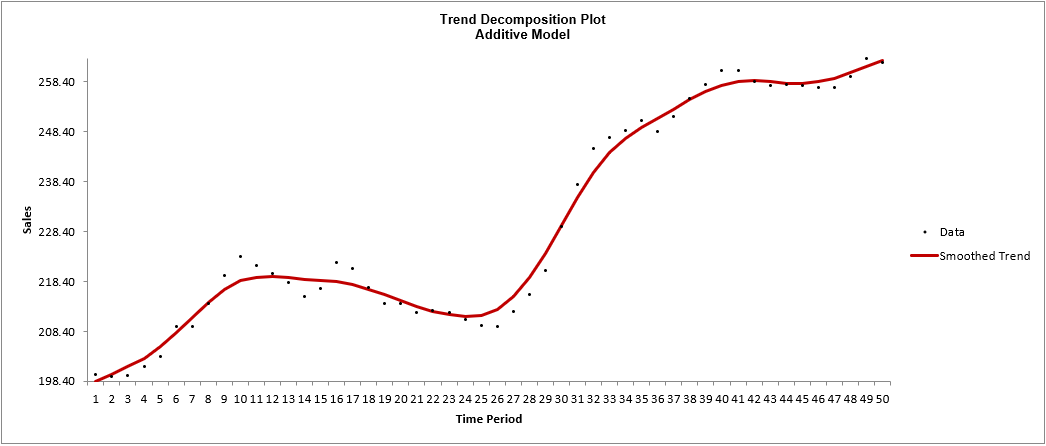

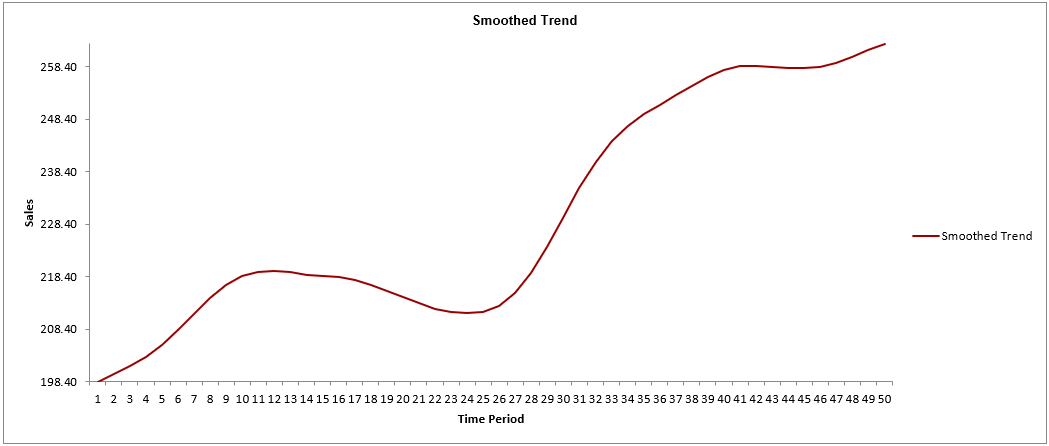

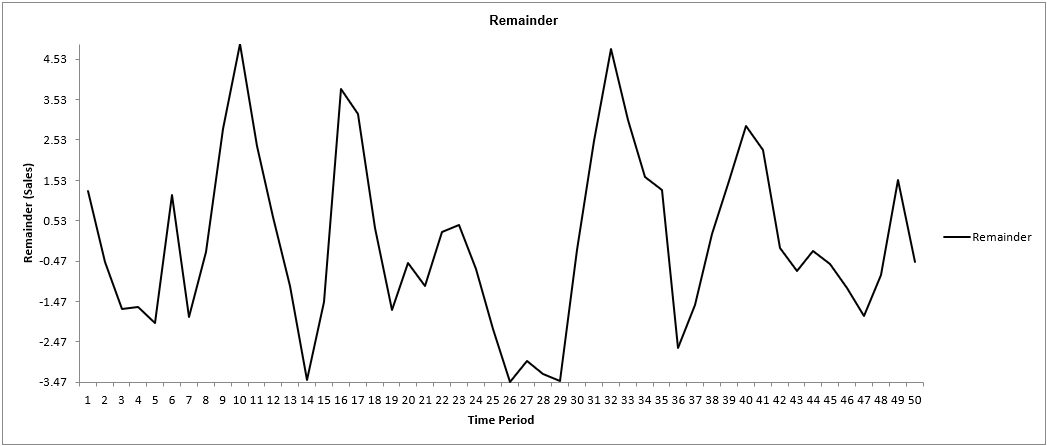

Sales with Indicator - Modified Series M

Open Sales with Indicator - Modified Series

M.xlsx. (Sheet 1 tab). This is modified

Series M data from Box and Jenkins, with 50 quarters of corporate sales values along

with a leading

indicator. The data is treated as nonseasonal, as done in Box and Jenkins.

Click SigmaXL > Time Series Forecasting > Seasonal

Trend Decomposition Plots. Ensure that the entire data table is selected.

If not, check

Use Entire Data Table. Click Next.

Select Sales, click Numeric Time Series Data (Y)

>>.

Seasonal Frequency and Box-Cox Transformation should

be unchecked as shown.

Click OK. A Trend Decomposition Plot for

Concentration is produced.

Here we see an overall positive trend over the 50 quarters.

The Smoothed Trend and Remainder Plots are also produced as

shown:

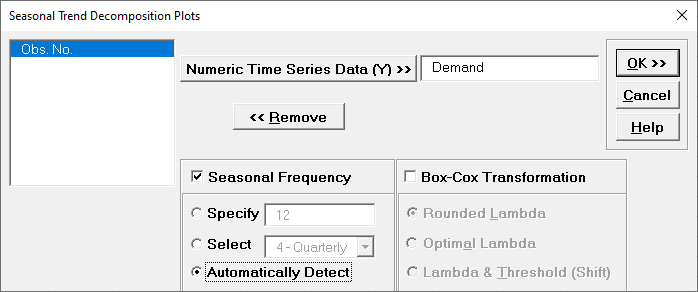

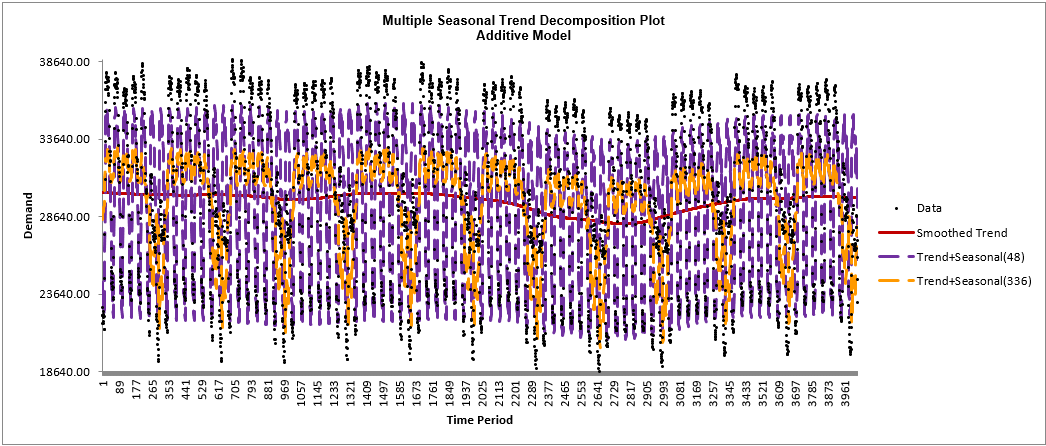

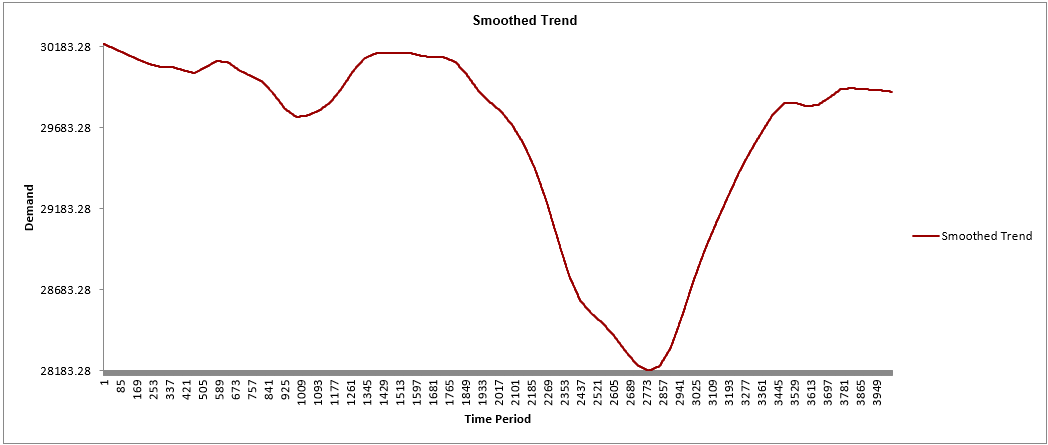

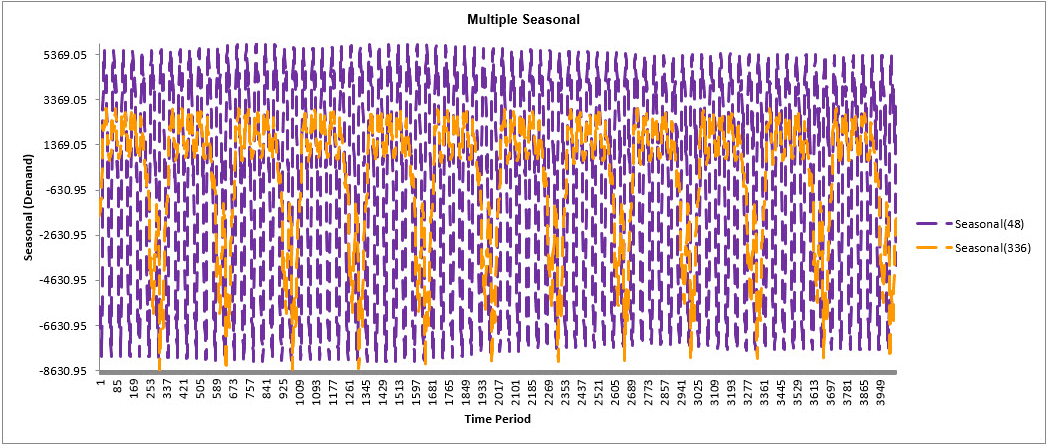

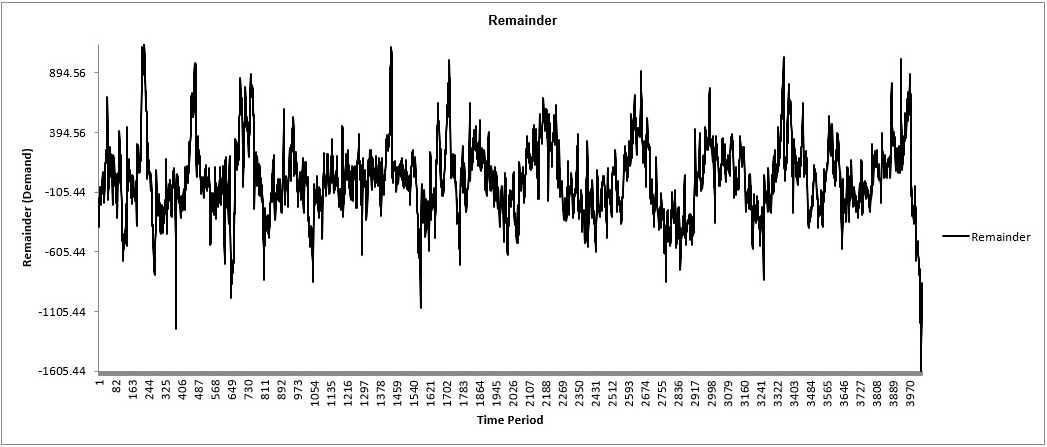

Half-Hourly Multiple Seasonal Electricity Demand Taylor

Open Half-Hourly Multiple Seasonal Electricity Demand -

Taylor.xlsx (Sheet 1 tab). This is halfhourly electricity

demand (MW) in England and Wales from Monday, June 5, 2000 to Sunday,

August 27, 2000 (taylor, R forecast). This data has multiple seasonality with frequency

= 48 (observations per day) and 336 (observations per week), with a total of 4032

observations.

Click SigmaXL > Time Series Forecasting > Seasonal

Trend Decomposition Plots. Ensure that the entire data table is selected.

If not, check

Use Entire Data Table. Click Next.

Select Demand, click Numeric Time Series Data (Y)

>>.

Seasonal Frequency with Automatically Detect. Uncheck

Box-Cox Transformation.

Click OK. A Seasonal Trend Decomposition Plot for

Demand is produced.

Automatic detection of seasonal frequency gives 48, 336, as obtained earlier with the

Spectral.html. Here we see the half-hourly multiple seasonal effect with 48

observations per day

and 336 observations per week.

The Smoothed Trend, Seasonal and Remainder Plots are also produced

as shown:

The Seasonal Trend Decomposition Plots are useful to visually

distinguish trend and seasonal components in the time series data. If the Seasonal Frequency

is unchecked, a Trend Decomposition Plot is produced as the first chart, showing the raw

data and the trend. The trend component uses data smoothing, rather than a linear trend so

that it may display either a linear trend or cyclical patterns. If a single seasonal

frequency is specified, a Seasonal Trend Decomposition Plot is produced, showing the data,

smoothed trend and seasonal component. If a multiple seasonal frequency is specified, a

Multiple Seasonal Trend Decomposition Plot is produced, showing the data, smoothed trend and

multiple seasonal component.

The second chart shows just the smoothed trend; the

third chart (if applicable) shows just the seasonal or multiple seasonal component. The

final chart is the remainder component.

This is an additive decomposition model, so

the sum of the trend value + seasonal value(s) + remainder value gives the original data

value. A multiplicative equivalent may be obtained by specifying the Box-Cox Transformation

with Lambda = 0, which is a Ln transformation, but the charts will display the transformed

data to maintain an additive model. Rounded or Optimal Lambda may also be used, but will

only consider the range of values 0 to 1 (this conservative approach is used in time series

forecasting, unlike regular Box-Cox in SigmaXL which uses a range of -5 to 5). See Appendix:

Box-Cox Transformation.

The decomposition algorithms used here are the same as used

in Exponential Smoothing Multiple Seasonal Decomposition (MSD), and ARIMA MSD. The

seasonal component is first removed through decomposition, a nonseasonal exponential smooth

model fitted to the remainder + trend, and then the seasonal component is added back in.

This is mainly used for high seasonal frequency and/or multiple seasonal frequency time

series. For further details and formulas, see Appendix: Seasonal Trend Decomposition.