- LIVE HELP IS

ARIMA Multiple Seasonal Decomposition (MSD) Control Chart

- Open Monthly Airline Passengers – Modified for Control Charts.xlsx (Sheet 1 tab). This is based on the Series G data from Box and Jenkins, monthly total international airline passengers for January 1949 to December 1960. A Ln transformation is applied (avoiding the need for a Box-Cox transformation), a negative outlier is added at 50 (-.25) and a level shift applied (+.25), starting at 100. The Multiple Seasonal Decomposition (MSD) option is not necessary for this data, but by way of introduction, we will use this to compare to the previous analysis.

- Click SigmaXL > Time Series Forecasting > ARIMA Control Chart > Multiple Seasonal Decomposition Control Chart. Ensure that the entire data table is selected. If not, Use Entire Data Table. Click Next.

-

Select Ln(Airline Passengers-Modified), click

Numeric Time Series Data (Y) >>. Uncheck

Display ACF/PACF/LB Plots and Display Residual

Plots. Check Seasonal Frequency with

Specify = 12. Leave Specify Model

Periods and Box-Cox Transformation

unchecked.

- Click Model Options.

- We will use the default

Automatic Model Selection with AICc as

the Model Selection Criterion. Click OK

to return to the ARIMA Control Chart dialog. Click OK. The ARIMA

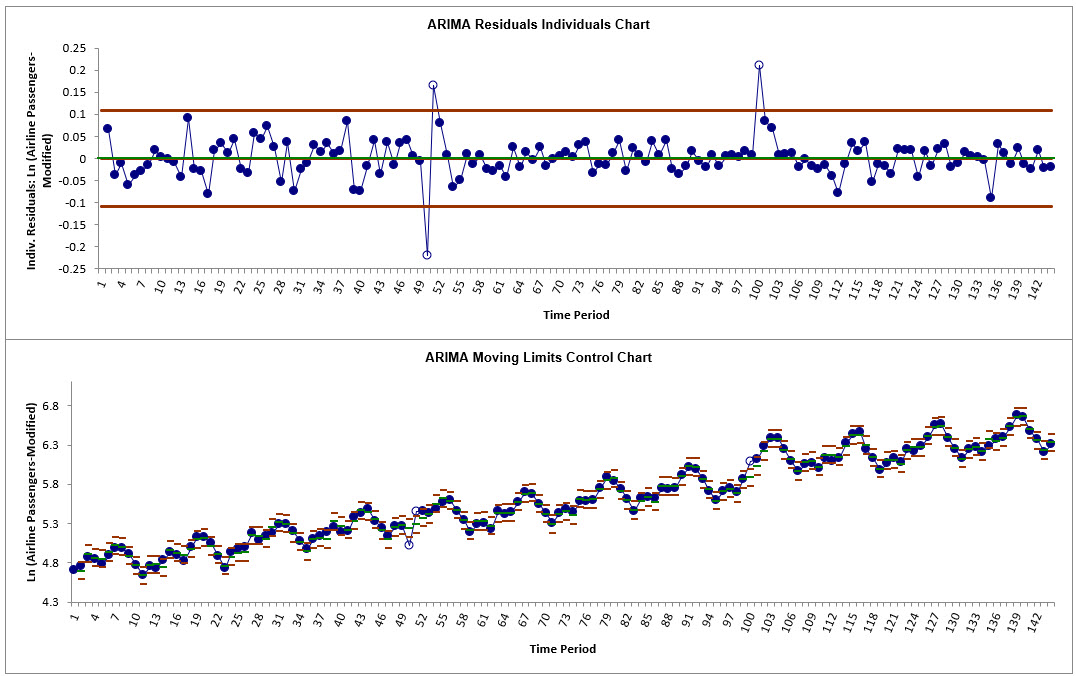

(MSD) control charts are produced:

We can clearly see the out-of-control data points at 50, 51 and 100 on the Residuals Individuals chart. This is similar to what we observed previously with regular ARIMA Control Charts. - Scroll down to view the ARIMA MSD Model

header:

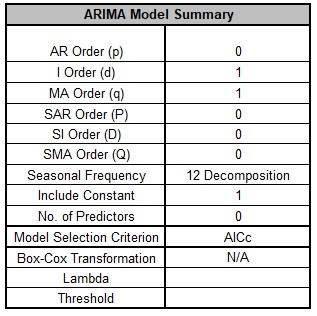

- The ARIMA Model Summary is given as:

This is a summary of the model information for the deseasonalized data: ARIMA (0,1,1) with a constant. Seasonal Frequency = 12 using Decomposition and Model Selection Criterion = “AICc”. There are no seasonal terms in the model. The Box-Cox Transformation is “N/A”.

This is a summary of the model information for the deseasonalized data: ARIMA (0,1,1) with a constant. Seasonal Frequency = 12 using Decomposition and Model Selection Criterion = “AICc”. There are no seasonal terms in the model. The Box-Cox Transformation is “N/A”. - We will not review the Parameter Estimates, Model Statistics and Forecast Accuracy as they are close to the ARIMA MSD values given earlier, although note that slight differences are due to the introduction of an outlier and a shift, as well now we are using all of the data, i.e., there are no withhold periods. Earlier we used a Box-Cox Transformation with Lambda=0 and here we are using Ln of the data.

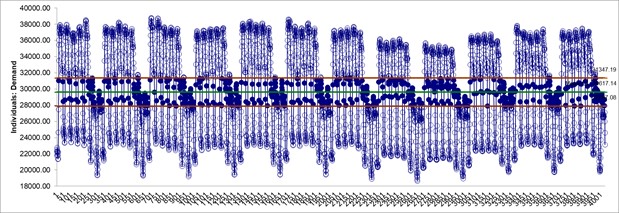

- Open Half-Hourly Multiple Seasonal Electricity Demand - Taylor.xlsx (Sheet 1 tab). This is half-hourly electricity demand (MW) in England and Wales from Monday, June 5, 2000 to Sunday, August 27, 2000 (taylor, R forecast). This data has multiple seasonality with frequency = 48 (observations per day) and 336 (observations per week), with a total of 4032 observations. See the Run Chart, ACF/PACF Plots, Spectral Density Plot and Seasonal Trend Decomposition Plots for this data.

- We will first construct a classical Individuals Control Chart on the raw data. Click SigmaXL > Control Charts > Individuals. Ensure that the entire data table is selected. If not, check Use Entire Data Table. Click Next.

-

Select Demand, click Numeric Data Variable (Y)

>>. Click OK. An Individuals Control

Chart is produced:

With the high frequency seasonality, this control chart is

meaningless.

With the high frequency seasonality, this control chart is

meaningless.

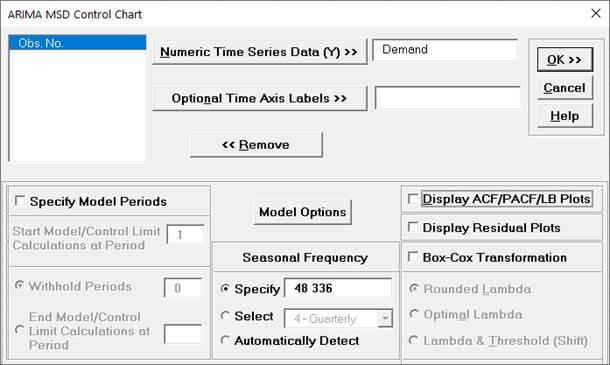

- Click SigmaXL > Time Series Forecasting > ARIMA Control Chart > Multiple Seasonal Decomposition Control Chart. Ensure that the entire data table is selected. If not, check Use Entire Data Table. Click Next.

- Select Demand, click

Numeric Time Series Data (Y) >>. Uncheck

Display ACF/PACF/LB Plots and Display Residual

Plots. Check Seasonal Frequency with

Specify = 48 336. Leave Specify Model

Periods and Box-Cox Transformation

unchecked.

- Click Model Options.

- We will use the default

Automatic Model Selection with AICc as

the Model Selection Criterion. Click OK

to return to the ARIMA MSD Control Chart dialog. Click OK. The

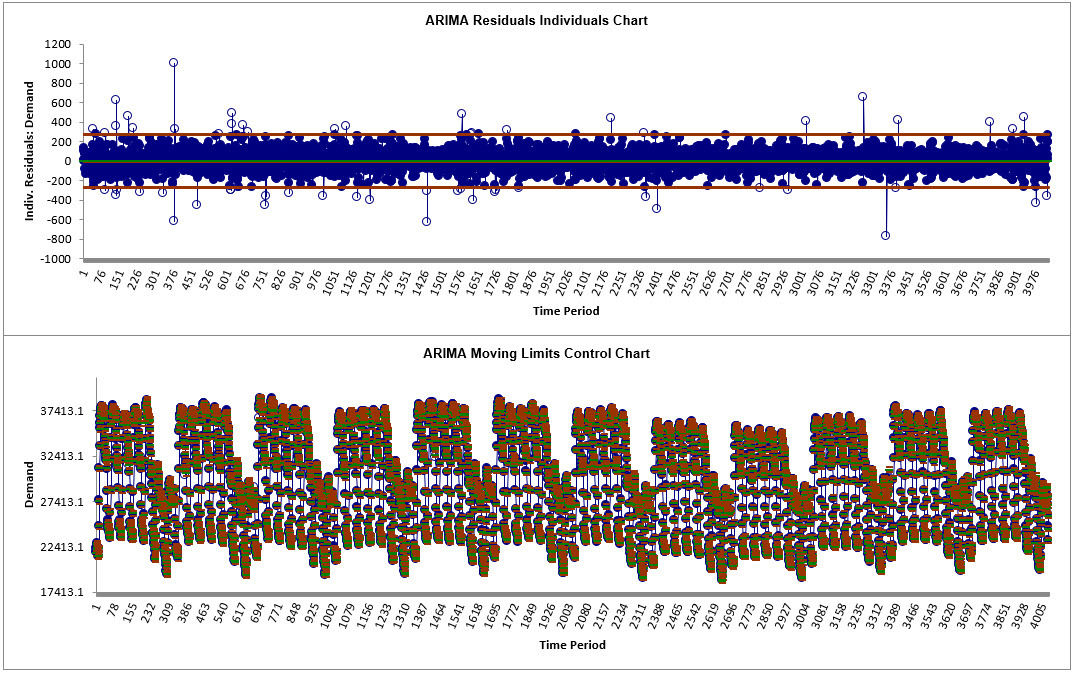

ARIMA MSD control charts are produced:

-

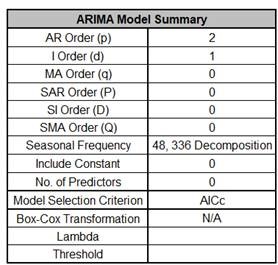

Scroll down to view the ARIMA MSD Model header:

-

The ARIMA Model Summary is given as:

- We will not review the Parameter Estimates, Model Statistics and Forecast Accuracy as they are close to the ARIMA MSD values given earlier, although note that now we are using all of the data, i.e., there are no withhold periods.

-

ARIMA does not have a theoretical

frequency limit, but for computational efficiency and to minimize

the potential loss of observations through differencing, we

recommend using ARIMA – Multiple Seasonal Decomposition (MSD) for

seasonal frequency greater than 52 (or with multiple frequencies).

The seasonal component is first removed through decomposition, a

nonseasonal ARIMA model fitted to the remainder (+trend), and then

the seasonal component is added back in. As the name

implies, Multiple Seasonal Decomposition (MSD) also accommodates

multiple seasonality, for example the half-hourly data with a

seasonal frequency of 48 observations per day and 336 observations

per week. An Individuals control chart of the residuals is

created for this forecast method. The Moving Limits chart uses the

one step prediction as the center line, so the control limits will

move with the center line. If a Box-Cox transformation is used then

an inverse transformation is applied to calculate the control

limits.

The popular “Add Data”, “Show Last 30” and “Scroll” features in SigmaXL Chart Tools are available for these control charts. For “Add Data”, the time series models are not refitted, but used to compute the residual values for the new data.

Define, Measure, Analyze, Improve, Control

Simulate, Optimize,

Realize

Web Demos

Our CTO and Co-Founder, John Noguera, regularly hosts free Web Demos featuring SigmaXL and DiscoverSim

Click here to view some now!

Contact Us

Phone: 1.888.SigmaXL (744.6295)

Support: Support@SigmaXL.com

Sales: Sales@SigmaXL.com

Information: Information@SigmaXL.com